Credit rating agency Moody’s has downgraded the foreign and local currency issuer ratings of the Government of Tanzania from B1 to B2 and changed the outlook from negative to stable.

Obligations rated B are considered speculative and are subject to high credit risk. Moody’s appends numerical modifiers 1, 2, and 3 to each rating. The modifier 1 indicates that the obligation ranks in the higher end of its rating; the modifier 2 indicates a mid-range ranking.

Rationale for Downgrade

Ongoing uncertainty over the regulatory environment and policy stance of the government, particularly as it relates to the mining sector, has a long-term negative impact on the country’s growth potential and ability to attract foreign investment, Moody’s explains.

The Government of Tanzania has been involved in a high-profile dispute with Acacia Mining, the county’s largest gold exporter, since 2017 when Tanzania banned the export of unprocessed metals, subsequently presenting Acacia with a USD 190 billion tax bill.

Eventually, Acacia’s largest shareholder Barrick Gold Corporation agreed to solve the dispute by paying a first tranche of the USD 300 million settlement.

Nonetheless, Moody’s stresses that slow and unpredictable government policy implementation continues to hinder the country’s investment attractiveness as evidenced by a thin pipeline of investment projects compared to other countries with high mining potential.

In the context of a general anticipated slump in FDI flows across the world as a result of the coronavirus outbreak, Tanzania’s policy unpredictability is likely to exacerbate the FDI shortfall.

The coronavirus outbreak and run-up to elections in October 2020 make unlikely, in the foreseeable future, any significant governance reforms to address policy unpredictability.

Policy unpredictability also contributes to fiscal and liquidity risks such as withholding aid funding by intentional donors.

This is likely to bring the country to rely on costlier non-concessional funding, and negatively impact the inflow of foreign investment, growth potential and the government’s fiscal strength and liquidity risks.

Moody’s notes that in turn, this will hinder Tanzania’s capacity to sustain high GDP growth rates, which is necessary to increase the economy’s shock absorption capacity.

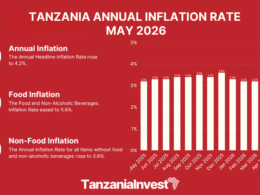

As a result, while Moody’s expects a modest deterioration in the fiscal balance to a 4.2% of GDP deficit in fiscal year 2020/2021 (the year ending on 30 June 2021), compared with an estimated 0.8% in fiscal year 2019/20, the higher financing needs will in large part be covered by more expensive non-concessional sources.

Rationale for Stable Outlook

The Tanzanian economy is relatively well diversified, driven by a mix of agriculture, manufacturing, construction, and services, as well as a robust GDP growth, averaging 6.7% between 2010 and 2019.

However, a relatively narrow revenue base, at around 15% of GDP, limits the government’s debt carrying capacity.

The relatively moderate fiscal deficits of 1.5% of GDP on average over the last three years mask challenges on revenue mobilization and arrears accumulation.

Additionally, environmental, social and governance considerations are central to Tanzania’s economic growth and credit profile:

- Environmental: Given the central place of agriculture within the Tanzanian economy, and reliance on rainfall to drive irrigation and hydroelectric plants, recurring droughts can have a significant negative impact on the agriculture and energy sectors.

- Social: Tanzania suffers from low wealth levels, income inequality, and high levels of poverty which constrain its development. Access to quality basic services such as education, healthcare and access to roads and general infrastructure is a challenge. Moody’s regards the coronavirus outbreak as a social risk under its ESG framework, given the substantial implications for public health and safety.

- Governance: Unpredictable policy actions weaken the government’s interaction with the private sector. Additionally, the government’s inability to fully implement its budget also weighs on Moody’s view of government effectiveness.

Want to know more about the Economy in Tanzania? Our free overview of the Tanzania Business and Investment Guide 2026 covers the Economy, plus key sectors and investment opportunities. The complete 141-page edition includes policies, taxation, key regulations, full macroeconomic data, and sources.

Download Free OverviewGet the Full Guide