TanzaniaInvest had the pleasure of interviewing Ineke Bussemaker, MD and CEO of the National Microfinance Bank (NMB), Tanzania.

NMB is one of the biggest commercial banks in Tanzania, 32% of which is owned by the government.

Bussemaker talks about the current lack of liquidity in the banking sector, the country’s investment potential and economic outlook.

TanzaniaInvest (TI): Tanzania is among the top African destinations for FDI. What is your view on the country’s potential and framework for investments?

Ineke Bussemaker (IB): Tanzania, as well as Kenya and Cote d’Ivoire, are the top African countries that investors are very interested in.

The investment appetite for Tanzania is largely driven by its size with 50m people but the country is still quite underdeveloped so there is high growth potential, especially in agriculture.

However, Tanzania is struggling to transform that potential and ideas into practical projects.

This is due to a range of issues that Tanzania has to solve.

One is political decision-making: it is taking investors a very long time between their first visit to Tanzania and the time when they reach an agreement with any government entity.

TI: In which sectors in Tanzania do you see the highest potential for growth?

IB: Tanzania’s largest potential is hiding in agriculture and particularly in the agro-processing industry.

However, the sector is dominated by smallholder farmers, which is somewhat limiting in terms of size of the investments.

I believe that medium or large commercial farms will help Tanzania to develop, because these farms will also create infrastructure.

Accordingly, there will be power, water, and means of transportation.

Large farmers have the advantage of scale, and the small farmers can benefit from it.

For example, there are 7,000 smallholder farmers benefiting from the infrastructure of the Kilombero Plantations (KPL), a farm in the Kilombero Valley, charged with developing over 5,800ha of land.

I strongly believe in this model and I think that Tanzania can make significant progress by applying it.

At NMB, we work with farming cooperatives and farmer groups, providing them with loans and working capital as well as training / capacity building by NMB Foundation.

TI: Which other sectors of the Tanzanian economy have the greatest realistic potential for growth?

IB: I believe that Tanzania’s gas, helium, energy, and construction sectors also have great potential for growth.

The government is very focused on building infrastructure, including roads, schools, and health clinics, and so, the building sector is growing especially in the rural areas.

Tanzania is also endowed with large mineral resources, which will continue to support the country in the future.

Also, the potential of Tanzania to double its population from 50 to 100m people in the next few decades is calling for industrialization.

TI: Tanzania is currently experiencing a lack of liquidity in the market. What are the reasons behind this situation and how is this impacting your balance sheet?

IB: Part of the liquidity was in the banking system, but the government has asked all of that to be transferred to Bank of Tanzania (BOT), especially the deposits from parastatals and local governments.

So, in the last few months there has been a shortage of liquidity in the market, which in turn impacts our capacity to lend and our balance sheet significantly.

We have tried to mitigate these effects by using other funding sources.

These include our own bond issue and longer-term funding from the Netherlands Development Finance Company (FMO) and The European Investment Bank (EIB).

However, these sources of funding are more expensive, resulting in higher interest rates on loans, which is not conducive to a growing economy.

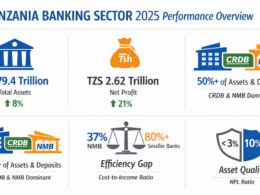

TI: According to NMB’s results for Q3 2016, net income after tax increased by 8.5% over the period, and by 9% in the cumulative year. What has been the driver of this growth, considering that other large banks are showing losses for Q3?

IB: The driver of our growth has been stability with a solid and growing customer base.

In addition, over the last 3 years, we have completely renovated our entire branch network and provided better IT services to all of our customers.

This attracts new customers, and at the same time, we have trained our staff in the branches to become more customer-sales focused.

TI: In Q3 2016 several Tanzanian banks have shown high percentages of Non-performing Loans (NPLs), above the 5% threshold set by the Bank of Tanzania (BOT). What is the situation at NMB?

IB: The percentage of NPLs at NMB is around 3%.

We have invested a lot in our credit-scoring systems, and we are also using the credit bureaus that were recently introduced.

And after the loans are approved, we conduct a proper follow-up with our customers.

However, we also foresee that some businesses that we support will default on their loans because of the current challenging environment.

TI: Tanzania’s banking penetration is limited; however the use of mobile money is widespread. How is fintech impacting your expansion strategy in light of the fact that you have the largest banking network in the country?

IB: In Tanzania roughly 15% of the 50m population have a bank account, while 30m people have a mobile phone, and potentially use a mobile wallet.

So, there are at least 20m more potential customers for us in the market that we can reach with digital technology, which is scalable, cheaper, and far more reachable.

We will never reach those 20m in a scalable, profitable way, through our branch network.

TI: Does this mean that you’re not going to open new branches?

IB: NMB is partly owned by the government and when it is establishing new districts, which need banking services, we consider opening a branch.

But if we can work with agents and through digital services instead of opening a branch, that would be our preference.

Overall, our vision is to make the whole value chain digital, building credit history and historical data, so that businesses and individuals can get microloans based on the transaction history in the use of digital services.

TI: The Tanzanian market includes 60 banks and other financial institutions. Do you foresee new players coming into the market or consolidation taking place?

IB: In my opinion a healthy banking sector is comprised of a smaller number of stable banks, and I think 60 banks are a bit too many.

In addition, the investments that banks need to make in modern and digital technology, might be overwhelming for small banks.

So, yes, I foresee a consolidation in Tanzania’s banking sector.

TI: Tanzania is on its path of becoming a middle-income country by 2025. For this, it needs a GDP growth of 10% against the current growth of 7%. Is this feasible in your opinion?

IB: The government’s ambition of reaching a GDP growth higher than the current 7% keeps me optimistic.

The plans are in place, but Tanzania needs to speed up the execution process, which will require better collaboration between the government and the private sector.

Want to know more about Banking in Tanzania? Our free overview of the Tanzania Business and Investment Guide 2026 covers Banking, plus key sectors and investment opportunities. The complete 141-page edition includes policies, taxation, key regulations, full macroeconomic data, and sources.

Download Free OverviewGet the Full Guide