Banking

Tanzania's Banking sector holds TZS 62,165.1 billion in total assets, representing 70.2% of the country's financial system, with 44 licensed institutions, 63.21 million Mobile Money subscriptions, and a non-performing loan ratio that fell to 2.8% by December 2025.

Banking is the largest component of Tanzania's financial sector, regulated by the Bank of Tanzania under the Banking and Financial Institutions Act 2006.

The system comprises 44 licensed banking institutions—including 34 commercial Banks alongside microfinance Banks, community Banks, development Banks, and specialized mortgage entities—operating with both local and pan-African players such as Ecobank and Mkombozi Commercial Bank.[4]

Total Banking assets reached TZS 62,165.1 billion in 2024, growing 14.6% year-on-year, while sector profitability advanced 39.3% and the NPL ratio continued declining to 2.8% by December 2025.[2][5]

Mobile Money—with 63.21 million active subscriptions in 2024—and a fast-growing fintech ecosystem are accelerating Financial Inclusion, supported by the third National Financial Inclusion Framework (NFIF 2023-2028).

Islamic Banking, microfinance with 62,232 providers, and the social security subsystem anchored by NSSF (National Social Security Fund) and PSPF (Public Service Pensions Fund) complete the sector, with Pensions and supplementary schemes holding TZS 21.4 trillion in assets.

The Bank of Tanzania actively manages foreign exchange reserves and oversees forex stability while advancing major systemic projects—including the rollout of the Tanzania Instant Payment System (TIPS), feasibility work on a central bank digital currency, and the new Non-Interest Banking Regulations 2025—that are reshaping the architecture of finance across the country.

Banking Sector

Tanzania hosts 44 licensed banking institutions—34 commercial Banks accounting for 97.3% of total banking sector assets, three community Banks, three microfinance Banks, two development Banks, one house financing company, and one mortgage refinancing company.[4]

Of the 34 commercial Banks, 12 are locally owned and hold 65.7% of commercial Bank assets, while 22 are foreign-owned holding 34.3%.

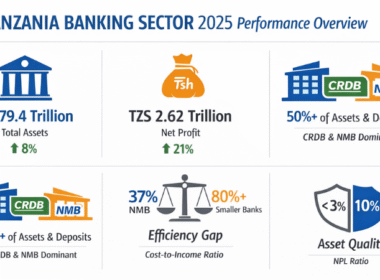

The two largest Banks—with significant Government shareholding—jointly account for nearly half of all banking assets, and the ten largest Banks held 79.4% of total assets, 82.4% of total loans, and 80.4% of total deposits in 2024.

Total assets reached TZS 62,165.1 billion in 2024 (+14.6% year-on-year), with loans, advances, and overdrafts at TZS 36,600.8 billion or 58.9% of total assets.[4]

Total profit hit TZS 2,129.0 billion in 2024 (+39.3%), with return on assets of 5.2% and return on equity of 23.7%; the leading Bank in 2025 reported ROA of 5.3% and ROE of 29.3%.[5]

The loan portfolio is led by personal loans at 37.2%, followed by trade at 12.5%, agriculture at 12.4%, and manufacturing at 9.6%.

The NPL ratio fell to 3.4% in 2024 from 4.4% in 2023, then further to 2.8% by December 2025.[2]

Lending rates averaged 16% in 2024 and 15% in 2025, while the overall deposit rate stood near 8%, and Q4 2025 credit to the private sector grew 17% year-on-year driven by trade and construction.

Service delivery expanded to 1,028 Bank branches in 2024 (from 1,011) supported by 145,430 banking agents, with Bancassurance emerging as a significant distribution channel for insurance products.

The BOT transitioned to an interest rate-based monetary policy framework in 2024, maintaining the Central Bank Rate at 5.75% for Q1 2026.

Microfinance

The Microfinance Act 2018 formalized the subsector by classifying providers into four tiers—Tier 1 deposit-taking microfinance Banks, Tier 2 non-deposit-taking providers, Tier 3 Savings and Credit Cooperative Societies (SACCOS), and Tier 4 Community Microfinance Groups (CMGs).

Tanzania had 62,232 licensed microfinance service providers at end of 2024, with Tier 4 CMGs accounting for 94.7% of the total and registering 22.0% growth.

CMG formalization has been instrumental in promoting Financial Inclusion among previously excluded urban and rural populations, enabling group access to banking services, savings habits, and mutually agreed-rate loans.

Fintech

Tanzania's fintech space spans mobile payments, digital loans, investments, and insurance, with a turning point in 2008 marked by the launch of M-Pesa by Vodacom, enabling mobile phone-based transfers and bill payments without a traditional Bank account.

By 2013, platforms began offering microloans and savings products, and in 2014 Tanzania implemented full interoperability among mobile money networks.

Mobile Banking platforms operated by commercial Banks complement mobile money operators, together forming Tanzania's digital financial services backbone alongside agent networks and ATMs.

The Bank of Tanzania is researching the feasibility of a central bank digital currency, with the assessment focused on population readiness, infrastructural requirements, and implications for national payment systems and monetary policy.[8]

On cryptocurrencies, 9.7% of adult Tanzanians were aware of crypto in 2023 and 1.7% were actively investing[7]; a National Cryptocurrency Technical Committee conducted a pilot assessment in Dar es Salaam and Zanzibar, with no specific regulation yet in place though President Samia Suluhu Hassan acknowledged in June 2021 that blockchain and digital assets represent the future of finance.

The Financial Sector Deepening Trust (FSDT) Tanzania highlights blockchain, AI, and digital currencies as drivers of further inclusion.[6]

Mobile Money

Mobile Money remains the dominant fintech segment in Tanzania, with providers including M-Pesa (Vodacom), Tigo Pesa, Airtel Money, and HaloPesa operating under full interoperability since 2014.

Active subscriptions reached 63.21 million in 2024, up 17.46% from 51.72 million in 2023.

Transaction volumes grew 26.73%, rising from 5,061.20 million to 6,413.94 million transactions, while transaction value grew 28.54% from TZS 154,705.77 billion to TZS 198,859.29 billion.[3]

Mobile Money has evolved beyond simple transfers to integrate merchant payments, utility payments, government collections, and cross-border remittances, with Bank-mobile money interoperability via the Tanzania Instant Payment System (TIPS) enabling seamless transfers between wallets and Bank accounts.

Islamic Banking

Islamic Banking operates under Sharia law, which prohibits interest (riba) and investments in activities deemed unethical or harmful such as alcohol production and gambling.

With approximately half of Tanzania's population Muslim, Islamic Banking is a rapidly growing segment, though Sharia-compliant products are available to clients of all faiths.

The first fully-fledged Islamic Bank began operations in Tanzania in 2011, and several major conventional Banks have since expanded portfolios with dedicated Sharia-compliant products.

Islamic deposits account for 3.0% of total banking deposits and Sharia-compliant financing represents 2.6% of total industry credit in 2025.[1]

The Banking and Financial Institutions (Non-Interest Banking Business) Regulations 2025 provide the dedicated regulatory framework for Islamic finance.

Pensions and Social Security

Social security total assets reached TZS 21,353 billion in 2024 (+13.4% from TZS 18,834 billion in 2023), equivalent to 7.6% of GDP.

Mandatory schemes include the NSSF (National Social Security Fund) and PSPF (Public Service Pensions Fund), operating Pensions, health insurance, and workers' compensation across public and private sectors.

Mainland Tanzania has 2,831,345 mandatory scheme accounts (up from 2,799,344 in 2023), with 139,235 accounts in Zanzibar (up from 135,787), while voluntary scheme participation also grew via informal sector outreach.

Member contributions stood at TZS 4,897.8 billion in 2024 (+11.8%), with investment assets at TZS 19,054.0 billion (+11.3%) and investment income at TZS 1,328.5 billion (+9.7%).

The portfolio is diversified across Government securities, bank deposits, real estate (17%), and equities (8%), with 99.8% held domestically.

The rate of return on the total investment portfolio reached 17% in 2024 (up from 9% in 2023), delivering a real return of 13.48% against inflation of 3.1%.

The pension fund funding ratio stood at 66.0% (above the 40% minimum) and the non-pension funding ratio at 4.1 times (above the 1.0 floor).

Policies

The Bank of Tanzania is the primary regulator under the Banking and Financial Institutions Act 2006, with capital adequacy minimums of 10% core and 12% total—both above which the sector remained in 2024.

BOT transitioned from monetary aggregate targeting to an interest rate-based monetary policy framework in 2024, holding the Central Bank Rate at 5.75% for Q1 2026, while the Anti-Money Laundering Regulations 2012 (amended 2019) govern compliance across all regulated entities.

The Microfinance Act 2018 categorizes providers into four tiers—Tier 1 microfinance Banks under standard banking laws, and Tiers 2-4 under specific rules including the Non-Deposit Taking Microfinance Service Providers Regulations 2019.

Fintech and payment systems are governed by the National Payment Systems Act, the 2015 mobile payment guidelines, and the Fintech (Regulatory Sandbox) Regulations 2024, while Islamic Banking is governed by the Banking and Financial Institutions (Non-Interest Banking Business) Regulations 2025.

The Financial Sector Development Master Plan 2020/21-2029/30 sets nine strategic priorities—Financial Inclusion, consumer protection, financial stability, long-term development finance, financial integrity, regional cooperation, research, capacity and ICT, and regulatory modernization.

The National Financial Inclusion Framework (NFIF 2023-2028) targets women, youth, MSMEs, smallholder farmers, fishers, and persons with disabilities; the previous framework lifted adult access to formal financial services from 86% in 2017 to 89% in 2023.

Social security is regulated under the Social Security Act and supervised by the Prime Minister's Office-Labour and Employment, with NSSF and PSPF as principal mandatory schemes, while a market-aligned Treasury bond coupon rate system was introduced in January 2025 to replace the fixed-rate system.

Investment Opportunities

MSME lending represents only 20.1% of total outstanding loans in 2024[9], yet SMEs contribute one-third of GDP and 40% of total employment — a wide gap inviting innovative lending models, alternative credit scoring, and risk management solutions.

With 62,232 microfinance providers in the market, there is strong demand for technology partners offering credit scoring, digital onboarding, and savings products tailored to Tier 4 community groups.

Islamic Banking and Takaful are emerging growth segments, supported by Tanzania's large Muslim population and the 2025 Non-Interest Banking Regulations covering Sharia-compliant lending, deposits, sukuk, and Takaful underwriting.

Fintech entry points span mobile payments, digital lending, micro-savings, micro-investments, and white-label mobile banking platforms targeting underbanked segments through regulatory sandbox pathways.

Bancassurance already routes 37.7% of intermediary gross written premiums through banks, leaving meaningful room for insurers and digital distribution partners to expand product reach.

Mobile money opens cross-border remittance corridors, merchant acquisition, and micro-savings products built on interoperable national payment rails, while central bank digital currency feasibility work creates early entry points for technology and infrastructure partners.

Pensions asset management — with TZS 19 trillion in investment assets concentrated in government securities and real estate — presents opportunities for fund managers, custodians, and alternative-asset originators in corporate bonds and infrastructure.

Last Update: May 2026

References

- https://www.bot.go.tz/Publications/Regular/Annual%20Report/en/2026022607584561.pdf (Guide reference #1)

- https://www.bot.go.tz/Publications/Regular/Monetary%20Policy%20Statement/en/2026020710260034.pdf (Guide reference #47)

- https://www.bot.go.tz/Publications/Regular/Financial%20Stability/en/2025072310063848.pdf (Guide reference #106)

- https://www.bot.go.tz/Publications/Other/Banking%20Supervision%20Annual%20Reports/en/2025090116315713.pdf (Guide reference #107)

- https://www.tanzaniainvest.com/wp-content/uploads/2026/03/Tanzania-banking-sector-Analysis-2025-By-AML-Finance.pdf (Guide reference #108)

- https://www.fsdt.or.tz/2024/11/29/digital-financial-services-and-financial-technology-in-tanzania/ (Guide reference #109)

- https://www.fsdt.or.tz/wp-content/uploads/2023/07/FinScope-Tanzania-2023-Full-Report-Insights-that-Drive-Innovation.pdf (Guide reference #110)

- https://www.pwc.co.tz/press-room/navigating-uncharted-territory.html (Guide reference #111)

- https://www.bot.go.tz/Publications/Regular/Annual%20Report/en/2025082509110517.pdf (Guide reference #121)

Want to know more about Banking in Tanzania? Our free overview of the Tanzania Business and Investment Guide 2026 covers Banking, plus key sectors and investment opportunities. The complete 141-page edition includes policies, taxation, key regulations, full macroeconomic data, and sources.

Download Free OverviewGet the Full Guide