At its meeting held on 2nd July 2026, the Monetary Policy Committee (MPC) of the Bank of Tanzania raised the Central Bank Rate (CBR) from 5.75% to 6.25% for the third quarter of 2026.

The decision aims to contain inflation driven by high energy, fertilizer, and transportation costs in the world market, triggered by the geopolitical conflict in the Middle East.

Global economic activity weakened in the quarter ending June 2026, as the conflict disrupted energy supplies and trade routes, raising oil, fertilizer, freight, and insurance costs.

The MPC is confident that the CBR adjustment is sufficient to keep inflation within the target range of 3-5%, while continuing to support economic growth.

The policy stance is expected to be reinforced by moderate food inflation, supported by adequate food supply from the 2025/26 harvests.

In addition, the pass-through effect of the exchange rate to inflation is expected to be minimal, supported by high export earnings from gold, tourism, and agricultural commodities in the second half of 2026.

Economic Performances

The ongoing geopolitical conflict in the Middle East continues to pose risks to the domestic economy, though growth remained strong in the first half of 2026.

GDP

Real GDP growth in Mainland Tanzania is estimated at around 6% in the first half of 2026, underpinned by solid performance in agriculture, construction, mining, financial services, and transport activities.

The Zanzibar economy is estimated to have grown by 6.6%, primarily driven by tourism and construction.

Growth in the second half of the year is projected to remain above 6% in both economies.

Inflation

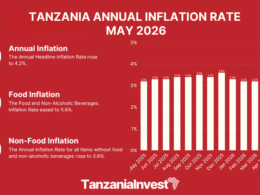

Annual headline inflation in Mainland Tanzania rose to 4.2% in May 2026, from 3.2% in March 2026, remaining within the target range of 3-5%.

A fuel subsidy provided by the Government in May and June helped to moderate the increase in inflation.

In Zanzibar, inflation reached 5.5%, up from 4.9%, compared with the target of 5%.

Inflation is projected to remain within target, despite facing elevated external risks.

Credit Supply

Private sector credit growth was robust, averaging 24% in the second quarter of 2026, supported by sustained demand from productive sectors.

The financial sector remained stable and resilient to shocks, with the banking sector remaining profitable and holding capital buffers sufficient to withstand short-term shocks.

Asset quality remained strong, with the non-performing loans ratio at 2.9% in May 2026, compared with the tolerable threshold of 5%.

Payment systems continued to operate smoothly and efficiently.

External Sector

The current account deficit was estimated at 2.4% of GDP in the year ending June 2026, compared with 2.2% in the year ending March 2026, and is projected to remain at the same level.

The Zanzibar economy sustained a current account surplus, driven largely by tourism receipts.

Forex

Foreign exchange reserves remained adequate at around USD 6 billion, sufficient to cover 4.3 months of projected imports, in line with the country’s minimum threshold of 4 months.

Reserves are projected to increase, supported by rising exports and continued accumulation of gold through the domestic gold purchase program.

Fiscal Performance

Fiscal performance was satisfactory, reflected in strong tax revenue collection alongside prudent expenditure and debt management.

Domestic revenue collection in 2025/26 is estimated to reach 16.8% of GDP, up from 15.6% in 2024/25.

Want to know more about Banking in Tanzania? Our free overview of the Tanzania Business and Investment Guide 2026 covers Banking, plus key sectors and investment opportunities. The complete 141-page edition includes policies, taxation, key regulations, full macroeconomic data, and sources.

Download Free OverviewGet the Full Guide