Microfinance

Tanzania's licensed microfinance service providers reached 62,232 at the end of 2024, following the formalization of the subsector under the Microfinance Act of 2018.

Microfinance in Tanzania delivers financial services to low-income individuals traditionally excluded from conventional banking, and forms part of the banking segment that accounts for 70.2% of total financial sector assets[1].

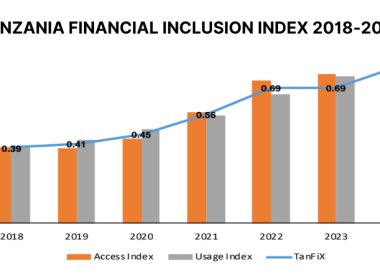

The subsector has become a central engine of financial inclusion, with expanded access points, mobile money integration, and community-based groups pushing the Tanzania Financial Inclusion Index (TanFiX) from 0.69 in 2023 to 0.81 in 2024[3].

Contents

Structure of the Microfinance Subsector

Microfinance provides financial services to low-income individuals who are traditionally not served by conventional financial institutions.

The formalization of the subsector in Tanzania took place with the Microfinance Act of 2018.

Since then, the number of licensed microfinance service providers has continued to increase, reaching 62,232 at the end of 2024.

The Microfinance Act categorized institutions into four tiers: Tier 1 covers deposit-taking microfinance service institutions (microfinance banks); Tier 2 covers non-deposit-taking microfinance service providers, such as individual money lenders; Tier 3 covers Savings and Credit Cooperative Societies (SACCOS); and Tier 4 covers Community Microfinance Groups (CMGs).

Banking, which includes microfinance and fintech, is the largest component of Tanzania's financial system, accounting for 70.2% of total assets, followed by social security at 24.1%[1].

Tier 4 Community Microfinance Groups Lead Growth

In 2024, Tier 4 microfinance service institutions accounted for 94.7% of the total, registering a strong growth rate of 22.0%.

The registration of these Community Microfinance Groups has played a significant role in promoting financial inclusion.

CMG formalization has been particularly effective in reaching populations that were previously excluded from formal financial services in both urban and rural areas.

By formalizing CMGs to operate as legal entities, the subsector is bringing informal savings and lending groups under a regulated umbrella.

Microfinance and Financial Inclusion

By 2024, notable progress was recorded in expanding financial access points, particularly mobile money and banking agents, microfinance institutions, and community microfinance groups.

This expansion was supported by improved ICT infrastructure, national identification interoperability, and rural electrification.

These developments contributed to a strong rise in the Tanzania Financial Inclusion Index (TanFiX) from 0.69 in 2023 to 0.81 in 2024[3].

Usage of financial services rose from 65% to 76% over the same reporting period.

The increase was mainly attributed to high adoption of digital financial services, greater awareness of financial products, and strong collaboration among public and private stakeholders.

Financial Sector Stability and Microfinance

The Bank of Tanzania (BOT) stresses that the financial sector, including banks, social security schemes, insurance, capital markets, and microfinance sub-sectors, remained sound and well-capitalized in the financial year 2024/25.

Asset quality and profitability improved, with sufficient buffers to absorb domestic and global shocks, and all performance indicators stayed firmly within the prescribed thresholds[1].

The Financial System Stability Index (FSSI) improved to 0.3 in June 2025 from 0.2 in the previous year.

This positive trajectory was driven by the sustained soundness of the banking sector, a favorable macroeconomic environment, and prudent risk management practices.

MSME Lending Gap

In 2024, MSME loans (including those accessed via personal credit) made up only 20.1% of total outstanding loans in banks and microfinance institutions, indicating a persistent finance gap[4].

Small business owners face barriers accessing credit due to widespread informality, lack of collateral, low financial literacy, and high costs, and often resort to personal loans.

While personal loans dominate private sector lending, they largely represent credit extended to SMEs[2].

This gap restricts growth and leaves businesses vulnerable to shocks.

It presents a clear opportunity for investors and financial service providers to develop innovative lending solutions, alternative credit assessments, and tailored risk management tools.

Policy and Regulatory Framework

Microfinance Act 2018

The Microfinance Act 2018 classifies providers into four tiers.

Tier 1 is regulated under standard banking laws, while Tiers 2 through 4 operate under specific rules such as the Non-Deposit Taking Microfinance Service Providers Regulations 2019.

BOT Oversight

BOT serves as the primary regulator for the financial sector, including banks, financial institutions, microfinance, Islamic finance, fintech, and payment systems.

Regulation is delivered primarily through the Banking and Financial Institutions Act, 2006, and its associated regulations.

This overarching framework is supported by the Anti-Money Laundering Regulations (2012, amended 2019), which ensure compliance across all regulated sectors.

Alignment with National Development Plans

The National Financial Inclusion Framework (NFIF) supports the implementation of national development plans, including Tanzania Development Vision 2050, the National Five-Year Development Plans, and the Financial Sector Development Master Plan 2020/21, 2029/30.

The NFIF aims to ensure all adults and businesses have access to and use a broad range of affordable and high-quality financial products and services.

Specific interventions focus on expanding access for women, youth, MSMEs, smallholder farmers, fishers, and persons with disabilities.

Investment Opportunities in Microfinance

Opportunities exist in digital banking, mobile payments, microfinance, and insurance services, with regulatory reforms supporting foreign investment in the financial sector.

Banks and fintech startups are driving financial inclusion across both urban and rural areas.

The MSME finance gap, with only 20.1% of outstanding loans reaching small businesses in 2024, creates room for innovative lending solutions, alternative credit assessments, and tailored risk management tools[4].

The rapid growth of Tier 4 Community Microfinance Groups, expanding at 22.0% in 2024 and now comprising 94.7% of all licensed providers, indicates strong demand for capacity-building, digital platforms, and integration services that connect informal savings groups to formal financial infrastructure.

Islamic finance is experiencing strong global growth, and Tanzania is part of this trend, with a large Muslim population and a growing offering of Islamic banking, investment, and insurance products meeting rising local appetite.

Rising incomes, improved ICT infrastructure, and national identification interoperability provide the foundation for scaling digital microfinance products to underserved rural and urban segments.

Last Update: May 2026

References

- https://www.bot.go.tz/Publications/Regular/Annual%20Report/en/2026022607584561.pdf (Guide reference #1)

- https://www.bot.go.tz/Publications/Regular/Monetary%20Policy%20Statement/en/2026020710260034.pdf (Guide reference #47)

- https://www.bot.go.tz/Publications/Regular/Annual%20Report/sw/2025082509110518.pdf (Guide reference #119)

- https://www.bot.go.tz/Publications/Regular/Annual%20Report/en/2025082509110517.pdf (Guide reference #121)

Want to know more about Microfinance in Tanzania? Our free overview of the Tanzania Business and Investment Guide 2026 covers Microfinance, plus key sectors and investment opportunities. The complete 141-page edition includes policies, taxation, key regulations, full macroeconomic data, and sources.

Download Free OverviewGet the Full Guide