The Bank of Tanzania (BoT) has released its 28th Banking Supervision Annual Report, presenting the performance of supervised financial institutions and developments in the financial sector for the year ending 31 December 2024.

The report indicates that the banking sector remained stable, well-capitalized, and profitable.

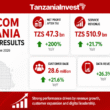

Total assets rose by 14.4% to TZS 62,203.8 billion in 2024 from TZS 54,396.0 billion in 2023, supported by higher deposits, borrowings, and earnings.

Deposits increased by 12.3% to TZS 42,772.1 billion, while loans, advances, and overdrafts grew by 14.3% to TZS 36,591.0 billion.

Profitability strengthened, with net profit up 39.3% to TZS 2,129.0 billion in 2024 from TZS 1,527.9 billion in 2023.

Return on assets increased to 5.2% from 4.4%, while return on equity rose to 23.7% from 20.5%.

Profit growth was driven by interest income from an expanding loan portfolio, higher non-interest income, and improved operational efficiency.

Capital adequacy ratios improved, with core capital at 19.4% and total capital at 20.0%, compared to 17.7% and 18.4% in 2023. Both remained well above the regulatory minimums of 10% and 12%.

Asset quality strengthened as the ratio of non-performing loans declined to 3.4% from 4.4% in 2023. Liquidity was stable, with the ratio of liquid assets to demand liabilities at 28.6%, above the 20% requirement.

The ratio of gross loans to deposits remained at 92.5%, showing banks continued to rely primarily on deposits to fund credit.

During 2024, the BoT approved several mergers and acquisitions to improve efficiency and compliance in the sector.

Kilimanjaro Co-operative Bank and Tandahimba Co-operative Bank merged to form Co-operative Bank Tanzania.

Access Bank (Nigeria) Plc acquired African Banking Corporation Tanzania and rebranded it as Access Bank Tanzania.

Selcom Paytech acquired Access Microfinance Bank, renaming it Selcom Microfinance Bank Tanzania. Exim Bank Tanzania acquired Canara Bank Tanzania.

The report highlights that the top ten banks continued to dominate the sector in 2024 in terms of assets, loans, deposits, and capital, benefiting from large customer bases and extensive branch networks.

Locally owned banks held 65.7% of commercial banking assets, while foreign-owned banks accounted for 34.3%.

The sector’s outreach expanded through branches, agent banking, and digital platforms.

Bank branches increased to 1,028 from 1,011 in 2023. Agent banking recorded strong growth, with the number of agents rising by 37% to 145,430.

Cash deposit transactions rose by 20.3% to 105.2 million, while cash withdrawals increased by 18.6% to 60.3 million.

Despite growth in distribution channels, agents remained concentrated in urban areas. Dar es Salaam accounted for 31.2% of all agents, followed by Mwanza (7.1%), Arusha (6.7%), Dodoma (5.3%), and Mbeya (5.0%).

On regulation, the BoT issued 765 licenses to non-deposit-taking microfinance service providers in 2024, while the Tanzania Cooperative Development Commission licensed 80 Savings and Credit Co-operative Societies (SACCOS), and local government authorities registered 10,642 community microfinance groups.

The central bank reaffirmed its commitment to enhancing anti-money laundering and countering the financing of terrorism frameworks, supporting the development of a regulatory and supervisory framework for Islamic banking, and integrating climate-related financial risk supervision.

The reportemphasized that the banking sector remains sound, resilient, and positioned to support economic growth through continued supervision, regulatory reforms, and collaboration with stakeholders.

Want to know more about Banking in Tanzania? Our free overview of the Tanzania Business and Investment Guide 2026 covers Banking, plus key sectors and investment opportunities. The complete 141-page edition includes policies, taxation, key regulations, full macroeconomic data, and sources.

Download Free OverviewGet the Full Guide