TanzaniaInvest interviewed Julius Ruwaichi CEO of Access Microfinance Bank Tanzania, a commercial bank focused on the lower and middle-income strata of the Tanzanian society and on the growing segment of micro and small enterprises.

In this interview, Ruwaichi provides a detailed insight on the issues affecting the vibrant Tanzanian baking sector, namely high-interest rates and non-performing loans, and shares his bank’s development strategy to become a leading provider of financial services in Tanzania with its large population, limited banking penetration, and plenty of opportunities to serve the unbanked.

Access Microfinance Bank Tanzania Limited is one of the six Access Group subsidiaries in Sub-Saharan Africa. How does it rank in terms of size and relevance?

Access Microfinance Bank Tanzania Limited (formerly AccessBank Tanzania Limited), was established in November 2007. We currently operate with a good network of branches in the Dar es Salaam, Mwanza, Mbeya, Tabora Iringa, and Kahama (Shinyanga).

As part of Access Group, our operation was the second next to Madagascar in the African space. The Bank managed to grow very fast and became the largest subsidiary of Access Group by 2017.

We attained good growth rates compared to other related players due to our active approach towards product development and market penetration rates in the segment where many local players had less experience and appetite to dwell in.

With subsequent internal and external challenges, together with the increase in the growth rate of other AccessGroup subsidiaries in markets, we are now the third in Africa in terms of total assets size, however, slowly regaining the growth to claim our leading position in the region.

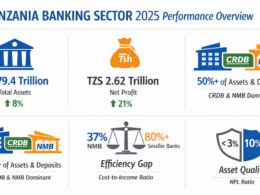

As of August 2021, the Tanzanian market is crowded with 35 commercial banks, 4 microfinance banks, and 575 tier 2 microfinance service providers. What are Access’ competitive advantages?

Access Microfinance Bank Tanzania is privileged with a well-crafted business model, which best fits the micro-segment in Tanzania. Our business model has been well tested for over 14 years across the wider geography of the country and hence forms part of DNA to a bigger slice of our workforce.

Access Microfinance Bank Tanzania is privileged with a well-crafted business model, which best fits the micro-segment in Tanzania.

We are excellent at servicing this segment in a manner that assures our customers a true meaning of progressive rewarding banking experience with business success. We are fast at understanding our customers’ business cycles, serving them with passion and recommendable turnaround time.

What new markets or initiatives are you pursuing?

Access Microfinance Bank Tanzania continues to walk its mission, intensify its presence where we are operating, while extending our services into new markets, with a focus of truly delivering on being a one-stop bank of choice for micro, agro, and small enterprises.

We have a special focus to widen the market share in serving the lower and middle-income strata of Tanzanian society.

We have a special focus to widen the market share in serving the lower and middle-income strata of Tanzanian society.

The bank continues to extend its presence in new rural areas, by reopening its historical and accessing new lending corridors, hand in hand with availing some of its banking services through agency banking and mobile banking services.

We have plans to embrace digital platforms to enhance our delivery as well as regain our market share from deep-rooted old clients and attract new clients.

Access to credit remains a challenge for Tanzanians, with historically high interest rates averaging 16% for commercial banks and 42% (3.5% per month) for microfinance institutions (from tier 2 to 4). What is your view on the Bank of Tanzania (BOT)’s cap on interest rates of a maximum of 3.5% monthly?

BOT, being the regulator of the banking industry in Tanzania, certainly had taken that measure with a wider view to achieving a certain regulatory objective, either on a short-term or medium-term basis.

It was a necessary measure taken at a particular time to achieve a certain governance framework. However, as a well-known engaging regulator, BOT has a number of channels for engaging the players in the sector to avail their ideas, which are rooted in operational dynamics.

As a matter of principle, interest rates are derived from a cumulative number of driving parameters. Hence, when all stakeholders are engaged to review and gain an understanding, reasonable rates can be justified.

It is our expectation that the position taken by the regulator has opened a wider room for more engaging discussions and submissions to give a wider scope on what needs to be addressed (drivers/parameters) to deliver market expected rates. Hence this might eventually lead to revisiting the initial position taken.

What does it take to lower the interest rates applied by banks?

As narrated above, lowering of interest rates applied by banks is a process-oriented result that has to be derived from engaging discussions of all stakeholders and players towards addressing the pricing drivers (that leads to the buildup of existing rates).

Currently, the Tanzania Bankers Association (TBA) is handling this diligently, engaging relevant players and stakeholders to get a clear understanding of the drivers and put sustainable measures that will enable players to comfortably allow market forces to dictate gradually reduced rates.

Which other measures would help unlock credit to Tanzanians?

In order to unlock credits to Tanzanians, it is important to look at wider and long-term views on the barriers that lead to limitations to credits:

- Borrowers’ creditworthiness information. It is high time for small to medium borrowers to institute mechanism of keeping financial records that are of credibility and reliability. This comes from education on the importance of keeping such information as well as discipline for them stand and deliver this. Having reliable financial reports helps banks to do a valuable assessment on borrower’s capacity, advising the best product/financial solution needed.

- Cost of funds. The majority of small and medium size borrowers do qualify for credit solutions offered by business models of Micro Finance Institutions (MFI) and Tier 1 Microfinance Banks, complemented by credits offered by commercial banks. However, most of these MFI have limitations in mobilizing financing, hence end up borrowing from financiers, commercial banks at relatively higher rates. This build up in the pricing equation, which might end up accommodating less borrowers. The preferable solution will be a coordinated joint effort for the MFI to borrow/access financing at relatively reasonable price, hence be able to extend relatively affordable credits to many more small and medium size Tanzanian businesses.

- Limited use of technologies. Many Tanzanians have access to mobile phones and internet. However, there are limited credit products developed and tailored to be made available to many players in Tanzania under the digital platform. More work needs to be done on the data collection/sharing and development of digital credit scoring algorithms. The evolution of Fintechs and innovations can help in unlocking credits for many Tanzanians, especially for small and short-tenured loans. This needs to go hand in hand with cultural change, trust, and financial discipline for the borrowers.

- Non-Performing Loans. The current level of non-performing loans at banking sector levels is close to 9%, with different banks at different levels of the ratio. However, it should also be highlighted that many banks have a significant amount of cumulative written-off loans based on statutory requirements. Therefore, the delays in recovering those overdue loans and collections from the written-off portfolio lower the appetite for more credits due to the capital implication (huge capital impact due to overdue).

After years of high non-performing loans ratios and the more recent impact of the Covid-19 pandemic, the banking sector has shown record profits in 2021 so far. How do you explain it?

Certainly, Covid-19 and the sticky trend of Non-Performing Loans (NPLs) have had a double sword impact on banks, as they led to a drop in revenues (fewer credit needs) and impairment charges. With many banks having extended the grace periods to their customers on repayment of loans installments, the impact has always been substantial.

The so-referred record in profits is contextual. In the recent past, banks had challenges on relatively higher impairments and declining credit growth or shrinkages for the majority of players. In 2021, the trend has relatively been contained, with the majority showing contained shrinkage, or small credit growth of their loan portfolio, hence stead growth in interest income and relatively lower impairment charges.

Therefore on a comparative basis, there has been growth. Furthermore, it is also worth noting that during the Covid-19 crisis, players were also poaching good clients from one another, hence record profits for an institution could also imply at the expense of other players who had to lose their good credit clients to other bigger players who could avail better terms at the difficult times.

Is this growth applicable to Access Microfinance Bank too?

Yes, for Access Microfinance Bank, there has been a positive trend as well, with the first nine months of 2021 closing with a loss before tax of TZS 0.3B, compared to last year for the same basis with TZS 9.2B. It is evident that we managed to grow our net interest income as well as contain our operating expenses, with an increase in recoveries of written-off loans for 2021.

We are determined to return back into profitability levels in 2022 as we cement our strategic focus in diligently serving the micro, agro, small and medium-size business segments.

We are determined to return back into profitability levels in 2022 as we cement our strategic focus in diligently serving the micro, agro, small and medium-size business segments.

According to your vision you “strive to be the leading provider of financial services in Tanzania.” How do you intend to do that, and what are the challenges ahead?

The journey is live and on its implementation. The banked population in Tanzania is just below 20%. Hence the banking opportunity is so immense here in Tanzania, and the micro-segment forms a bigger part of this.

Access Microfinance Bank is having a very robust business model to serve this clientele, as we have developed a very strong experience and DNA for over 14 years in this segment. We aim to continue partnering with players and engaging our clients to know their needs and tailor our products to best fit their needs as we always do.

The banked population in Tanzania is just below 20%. Hence the banking opportunity is so immense here in Tanzania

With the modern digital world, we will strive to keep pace by slowly transitioning with our clients into the digital space, while addressing the related risks with appropriate mitigations. This being a journal, we remain focused, less disrupted by the deliberate uproars.

We are aware of the challenges ahead, including dynamics of technologies, competitions, funding long-term funding needs, potential economic challenges, potential reoccurrence of the pandemic, etc. All these might be of impact to our journey, hence the continuous review of our strategies and adaptations remains key to us.

Want to know more about Banking in Tanzania? Our free overview of the Tanzania Business and Investment Guide 2026 covers Banking, plus key sectors and investment opportunities. The complete 141-page edition includes policies, taxation, key regulations, full macroeconomic data, and sources.

Download Free OverviewGet the Full Guide — USD 99