The Bank of Tanzania (BOT) has recently released its Annual Report 2019/2020 which covers, among others, annual economic developments in the country for the period ending June 2020.

In his foreword, the Bank’s Governor Prof. Florens Luoga recalls that in 2020, the BOT and the Governments took several measures to lessen or eliminate the possible negative impact of the Covid-19 pandemic on the Tanzanian economy.

The monetary policy measures introduced included lowering the statutory minimum reserve (SMR) requirement ratio by 100 basis points from 7.0% to 6.0% and cutting the discount rate by 200 basis points from 7% to 5.0%.

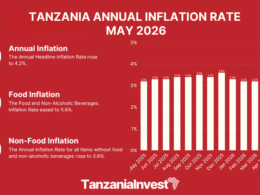

Worthy mentioning, credit to the private sector continues to grow amidst softening short-term interest rates; and stable, profitable, and adequately capitalized banking sector, and Tanzania continues to be among the fastest-growing economies in sub-Saharan Africa, with a real GDP growth of 7.0% in 2019, and moderate inflation averaging 3.5% in 2019/20.

Prof. Luoga stresses that to preserve these gains in the economy, the BOT seeks to maintain an accommodative monetary policy stance in 2021 while ensuring inflation remains within a range of 3 to 5%.

Policy direction will also be geared towards smooth functioning and stability of the financial sector and exchange rate, as well as strong growth of credit to the private sector.

Equally important is working with other stakeholders to take forward efforts to advance and accelerate financial development geared at enhancing access to and usage of financial services, Governor Luoga concludes.

Tanzania Monetary Policies in 2019/20

The conduct of monetary policy during 2019/20 remained accommodative in order to support the growth of credit to the private sector for supporting economic growth, while ensuring stability in money market interest rates.

This policy stance was strengthened by moderate inflation expectations and ongoing investments.

These measures were augmented by a reduction of haircuts on government securities pledged by banks for borrowing from the central bank window.

Want to know more about the Economy in Tanzania? Our free overview of the Tanzania Business and Investment Guide 2026 covers the Economy, plus key sectors and investment opportunities. The complete 141-page edition includes policies, taxation, key regulations, full macroeconomic data, and sources.

Download Free OverviewGet the Full Guide