The Tanzanian government will spend TZS 62.33 trillion (±USD 24 billion) in the fiscal year 2026/27, with 74.2% financed by domestic revenue and a deficit held at 3% of GDP, as foreign direct investment reached USD 21.7 billion in 2024.

The Minister for Finance, Ambassador Khamis Mussa Omar, tabled the consolidated Government Budget in Parliament in Dodoma on 11 June 2026, under the theme of building economic resilience through digital transformation, strategic investment, and fiscal sustainability.

The 2026/27 budget is the first under Tanzania Development Vision 2050 and the Fourth National Five-Year Development Plan (2026/27-2030/31). It is built on five priority areas: governance and stability, a competitive and inclusive economy, human capital, climate resilience, and transformative sectors.

The TZS 62.33 trillion budget represents a 10.3% increase over the TZS 56.49 trillion approved for 2025/26.

Total revenue is estimated at TZS 46.79 trillion (±USD 18.0 billion), comprising tax revenue of TZS 36.99 trillion, other revenue of TZS 9.24 trillion (including Local Government Authority own-source revenue of TZS 1.97 trillion), and grants from Development Partners of TZS 563.1 billion.

Approximately three-quarters of the budget, or 74.2%, will be financed through domestic revenue, in line with the government’s stated self-reliance objective.

Grants from Development Partners are projected to fall 39.1% in 2026/27 compared to the prior year, which the minister attributed to changes in Development Partners’ policies.

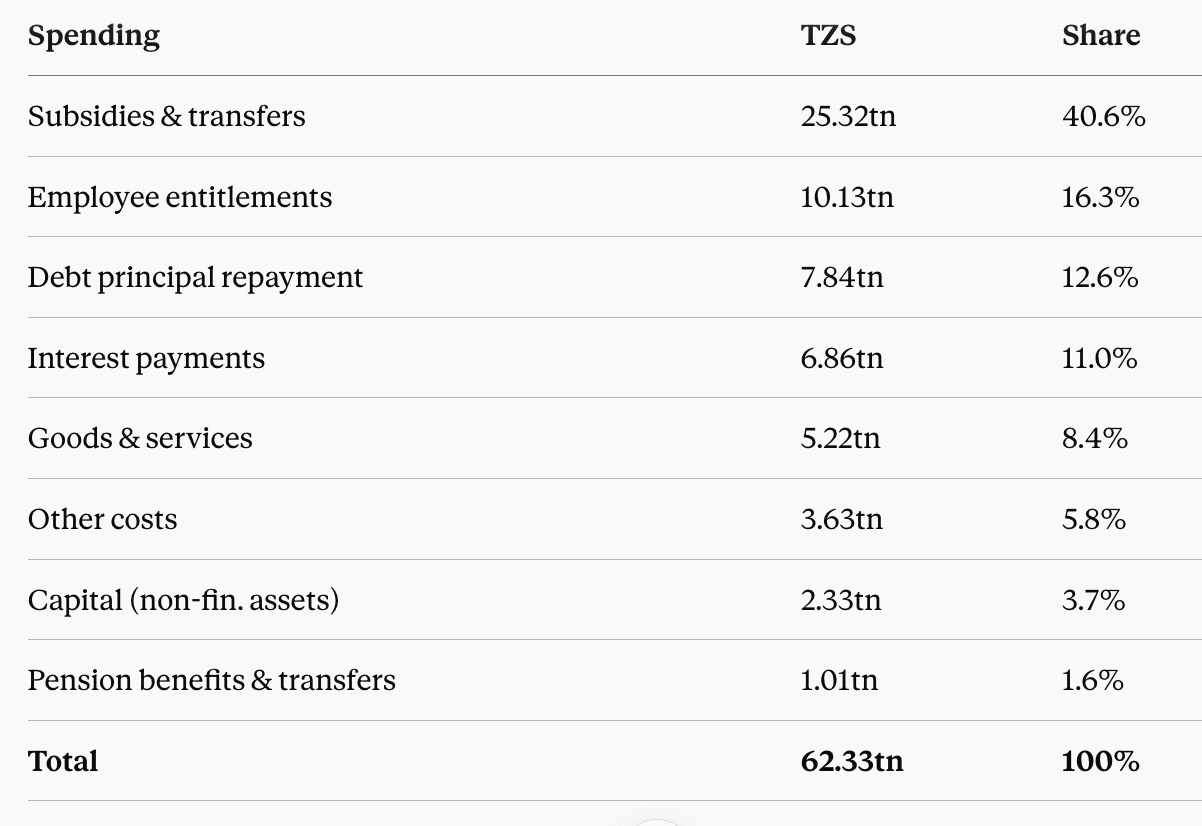

Tanzania 2026/27 Budget: Where The Money Goes

Expenditure and Deficit Financing

Expenditure and investment in non-financial assets are estimated at TZS 54.50 trillion (±USD 21.0 billion), excluding principal repayments on government debt.

The expenditure breaks down into employees’ entitlements including pension contributions of TZS 10.13 trillion, subsidies of TZS 25.32 trillion, interest payments of TZS 6.86 trillion, goods and services of TZS 5.22 trillion, other costs of TZS 3.63 trillion, investment in non-financial assets of TZS 2.33 trillion, and pension benefits and transfers of TZS 1.01 trillion.

The budget deficit is TZS 7.71 trillion, equivalent to 3% of GDP, which the government will finance through domestic and external borrowing under the Medium-Term Debt Management Strategy (2025/26-2027/28).

The government plans to borrow TZS 15.54 trillion in 2026/27, comprising domestic loans of TZS 6.56 trillion, external concessional loans of TZS 6.55 trillion, and external commercial loans of TZS 2.43 trillion. A further TZS 7.84 trillion is estimated for amortization of matured loans.

Macroeconomic Targets for 2026/27

Real GDP growth is targeted at 6.3% in 2026, up from 5.9% in 2025.

Inflation is to be contained within 3.0% to 5.0% over the medium term.

Domestic revenue is targeted to rise to 17.1% of GDP in 2026/27 from a projected 16.5% in 2025/26, and tax revenue to 13.7% of GDP from a projected 13.2%.

Foreign reserves are to be maintained at no less than four months of import cover.

2025 Economic and Budget Performance

Nominal GDP reached TZS 234.1 trillion in 2025, equivalent to USD 91.8 billion, and real GDP grew 5.9%.

Headline inflation averaged 3.4% from July 2025 to April 2026, within the medium-term target band.

Credit to the private sector grew by an average of 20.2% over the same period.

Foreign exchange reserves stood at USD 5,722.5 million as of April 2026, covering at least 4.4 months of imports.

The shilling appreciated against the US dollar by an average of 2.7% for the year ending April 2026.

Basic-needs poverty declined to 25.1% of the population, according to preliminary 2025 Integrated Household Budget Survey results, from 26.4% in 2017/18.

In 2025/26 to April 2026, the government collected TZS 34.75 trillion in revenue including grants, equivalent to 101.8% of the period target, with tax revenue at 105.1% of target.

In 2025/26 to April 2026, the government spent TZS 2.86tn on roads, bridges, and airports, TZS 1.59tn on electricity generation and transmission, and TZS 1.27tn on railway infrastructure including TZS 1.12tn for the SGR.

The Julius Nyerere Hydropower Project, generating 2,115 MW, was completed and launched, raising national power generation capacity to 4,522.54 MW. Through the Rural Energy Agency (REA), TZS 521.3bn was disbursed for rural electrification, connecting 39,003 hamlets.

The Dar es Salaam to Dodoma SGR segment (Lots 1 and 2) is complete and operational.

Government Debt and Credit Ratings

Government debt stood at TZS 114.34 trillion as of March 2026, comprising domestic debt of TZS 38.45 trillion (33.6%) and external debt of TZS 75.89 trillion (66.4%).

A Debt Sustainability Analysis conducted in November 2025 found the debt sustainable over the medium and long term. The present value of government debt to GDP is 39.6% against a threshold of 55%, external debt to GDP is 24.4% against a 40% threshold, and external debt to exports is 123.1% against a 180% threshold.

Moody’s Investors Service and Fitch Ratings completed a first-phase assessment of Tanzania’s debt-servicing capacity for 2026, with results indicating that Tanzania remains creditworthy with a strong capacity to service its debt obligations.

Strategic Investment and Sector Priorities

The government will expedite strategic investments in industries built on minerals and energy, specifically rare earth minerals, natural gas, iron ore, and coal, with an emphasis on domestic value addition to agricultural, fisheries, livestock, and mineral products rather than raw export.

Railway corridors anchor the investment agenda. The government will continue Standard Gauge Railway (SGR) construction on the Dodoma-Mwanza and Isaka-Kigoma sections, and implement the TAZARA Railway Revitalisation Project. The government identifies the corridors as direct opportunities to stimulate economic activity in the regions they cross, eight regions for the SGR and five for TAZARA.

Dodoma is to be developed beyond an administrative capital into a transport and logistics hub serving Tanzania and neighbouring countries, with the SGR and the new Msalato International Airport positioned as the enabling infrastructure.

A dedicated financing channel for industrial zones is introduced: 5% of designated revenue will be transferred to a special Bank of Tanzania account to fund infrastructure development in Export Processing Zones (EPZ) and Special Economic Zones (SEZ), including compensation for land acquired for SEZ establishment.

Several measures target value addition and protect domestic processing. A 30% export tax (or TZS 200 per kilogram, whichever is higher) is imposed on waste paper to retain raw material for local paper manufacturers, and a 10% export tax on quartz minerals.

Industrial development levies of 5% to 10% are imposed on imported steel structures, aluminium structures, and fishing nets to favour local production. Import duty relief is extended to local vehicle assemblers, including electric and gas vehicles, supporting the target of making Tanzania a leading African vehicle producer by 2030.

The apparel value chain receives continued protection, with import duties on cotton grey fabric and finished garments set to favour clothing produced from locally grown cotton.

The government will continue working with the International Finance Corporation (IFC), Africa50, Africa Finance Corporation (AFC), and the Asian Infrastructure Investment Bank (AIIB) to raise capital, guarantees, and technology for development projects.

Tax Measures

The government will reduce the share of taxable profit deemed distributed to shareholders (deemed retained earnings) from 30% to 15% under Section 33A of the Income Tax Act.

The reduction excludes the small financial sector, insurance companies, companies listed on the Dar es Salaam Stock Exchange (DSE), and institutions with Framework Agreements with the government.

New businesses will receive a one-year income tax exemption from the date of obtaining a taxpayer identification number.

The government proposes Value Added Tax (VAT) deferment to be maintained on imported capital goods to lower upfront investment costs.

VAT exemptions are proposed on Compressed Natural Gas (CNG) across the full distribution chain, on equipment for electric vehicle charging stations, and on imported LPG smart meters for distributors.

Import duty relief is proposed for vehicle assemblers and manufacturers, including those producing electric and gas-powered vehicles, under East African Community regulations.

A 1% non-final withholding tax is introduced on corporate purchases of food crops, and a 1% withholding tax on payments to sellers of live animals, unprocessed milk, and unprocessed fish, with purchasing companies acting as collection agents.

The presumptive tax rate rises from 3.5% to 4.5% for taxpayers with annual turnover between TZS 11 million and TZS 200 million.

New tax measures take effect on 1 July 2026 unless otherwise stated.

What Happens Next

The budget is not yet law. The Minister tabled the estimates for Parliament to debate and approve, alongside the Finance Bill 2026 and the Appropriation Bill 2026.

Parliament will debate the consolidated budget over the following sitting days. Approval requires passage of the Appropriation Bill 2026, which gives legal authority to spend, and the Finance Bill 2026, which enacts the tax measures.