The Monetary Policy Committee (MPC) of the Bank of Tanzania (BOT) met on 28th November 2022 to assess the recent implementation of monetary policy and economic performance.

On the basis of the assessment made, and given the spillover effects of the current global supply-side shocks on inflation and output, the MPC decided to continue lessening monetary policy accommodation in November and December 2022.

The policy decision is intended to align inflation expectations with the target while safeguarding the growth of economic activities. It also aims at facilitating the attainment of monetary targets for the quarter ending December 2022.

In addition, the MPC discussed the performance of the global economy and noted that it continued to be undermined by supply-side shocks. Based on this, the IMF forecasts growth to be lower in 2022 and 2023 than earlier projected.

Inflation also remained above targets in most countries, due to high commodity prices and climate-related challenges, prompting central banks to further tighten monetary policy.

Furthermore, the MPC noted that the outlook is uncertain, largely reflecting supply-chain disruptions caused by the war in Ukraine and climate-related challenges.

The MPC noted with satisfaction the recent implementation of monetary policy and

the performance of the domestic economy, despite being faced with a challenging global environment.

Specifically, the MPC observed that:

i. the manner in which monetary policy was implemented, and its outcome, were consistent with the plan. Liquidity in the banking sector was maintained at desirable levels consistent with the inflation forecast and monetary policy targets for the quarter ending September 2022 were successfully met;

ii. performance of the economy was on track. Growth in Mainland Tanzania was 5.2% in the first half of 2022, and the likelihood of realizing the projected growth of 4.7% for the whole year is high. Likewise, the Zanzibar economy grew at 5.8% in the first half of 2022, consistent with the projection of 5.4% for 2022. The economy is forecast to grow faster in 2023 than in the preceding year, as the spillover effects of the global shocks fade away;

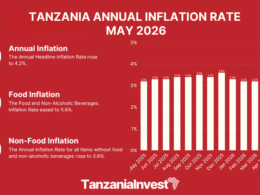

iii. inflation remained moderate, slowly rising due to the increase in prices of food and energy. In Mainland Tanzania, it reached 4.9 percent in October 2022, up from 3.8% in July 2021, but was consistent with the target of 5.4% for 2022/23. In Zanzibar, inflation rose to 7.3% from 2.2%, also broadly in line with the target of 5 percent. Inflation is expected to remain moderate and consistent with the target in 2022/23;

iv. money supply and private sector credit growth were on course. Money supply (M3) grew by 13.4% in October 2022, broadly consistent with the target of 10.3% for 2022/23. Private sector credit growth was high in September and October 2022, at 22 and 23.7%, respectively. In 2022/23, private sector credit growth is projected at 10.7%;

v. revenue performance was broadly on track in the first quarter of 2022/23. In Mainland Tanzania, revenue was 96% of the target, while in Zanzibar it was 98.5%. Expenditure also was on track, consistent with the rising needs to address the effects of global shocks and the infrastructure gap;

vi. the external sector of the economy remained sustainable but continued to be undermined by global supply-side shocks, which include high import prices and tightened financial conditions. Foreign reserves remained adequate, covering 4.2 months of imports, in line with the country benchmark of 4 months. The import cover is expected to increase, as world market prices of imports decline; and

vii. the banking sector performance was satisfactory. The sector remained liquid, capitalized, and profitable. Likewise, deposits and assets are increasing, and asset quality is improving. The non-performing loan ratio declined to 7.2% in October 2022, down from 8.3% in the corresponding period in 2021.

Want to know more about the Economy in Tanzania? Our free overview of the Tanzania Business and Investment Guide 2026 covers the Economy, plus key sectors and investment opportunities. The complete 141-page edition includes policies, taxation, key regulations, full macroeconomic data, and sources.

Download Free OverviewGet the Full Guide