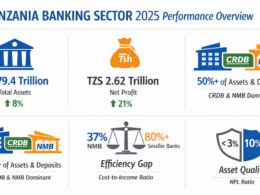

Outlook of the Tanzania Banking Sector

TANZANIAINVEST has been interviewing Mr. Israel Chasosa, Managing Director of the African Banking Corporation (ABC) Tanzania, to gather his vision and opinion about the country economic outlook and about its banking sector.

| Israel Chasosa, Managing Director of the African Banking Corporation Tanzania |

TI: How would you define the current situation of the banking sector in Tanzania?

Israel Chasosa – African Banking Corporation: There are quite a number of banks in Tanzania. At the moment we have 32 and I understand there are more to be registered.

I think banking is changing in Tanzania in the sense that the economy is growing and banks have to be innovative, aggressive and proactive in meeting the needs of such growing economy.

As a result, that is going to bring in a new breed of bankers.

Because we have so many banks, of course the margins are being squeezed and, therefore, banks have to open up in new areas.

I feel particularly the bigger banks are really going to change the way they do business in this country.

TI: Small and Medium Enterprises (SMEs) are expected to play a pivotal role in the further economic development of Tanzania. However, banks are said to be reluctant to lend to SME’s. What is your opinion on this subject?

IC: I believe that for SME’s to succeed in this country, there must be cooperation from different angles.

Definitely the rate of failure of SMEs has been high and that has put off some banks in taking an active role in financing this sector.

I think going forward we have to be pragmatic about this sector whereby banks need to come up with a way of helping the SMEs understand what they are required to do in order to qualify for loans.

At the same time the government must provide the enabling environment and to this extent something has been done with the current credit guarantee scheme.

This scheme has been set up through the central bank to assist those clients who cannot afford to provide collaterals, whereby the risk is shared between the government and the lending bank.

To me this is not enough though, in the sense that we need to educate the SMEs in first place.

So banks have a responsibility in the areas they operate otherwise it will be a recipe for disaster.

I think what is also lacking are role models to show shining example of SMEs that succeeded.

TI: The African Banking Corporation is one of the financial institutions in Tanzania taking part in this credit guarantee scheme. What are you doing for SMEs and how these fit with your target market?

IC: We have a main limitation in addressing SMEs that is the lack of branches of representation.

We only have one branch in Dar es Salaam.

Secondly, we did subscribe to that scheme for SMEs but our target market is rather medium size companies to large corporations and we are much more focused on these than in the past.

We look small but we are geared for big transactions

TI: What are you competitive advantages in this niche market?

IC: I think our biggest advantage is size and service.

We are small and we are very responsive to clients’ queries unlike the big banks where in my view there is too much bureaucracy.

We give personal customized service to all our clients because of our size and we are not going for volume, but for specific clients.

Our model is the same in every country we are.

We are a merchant bank, not a retail bank.

Tanzania Economy Future Growth

TI: What are your expectations on the economic growth of Tanzania and what are the biggest challenges this countries is faced with?

IC: This country has got a lot of potential and, as far as the African Banking Corporation is concerned, we are very optimistic about the future of its economy.

{xtypo_quote_right}This country has got a lot of potential and […] we are very optimistic about the future of its economy.{/xtypo_quote_right}It has a growing economy and as a result we want to tap in on new businesses and new opportunities from our existing clients as they expand.

I think the major challenges Tanzania faces are the energy crisis and the human resources skill base, which is growing though.

President Kikwete has actually publicly expressed that the government must allow the creation of a middle class, without which the economy cannot grow.

Such middleclass will be created only when there will be enough professionals.

Given a few years to come we will see the changes and the development around.

It is beginning to happen whereby, for example, in the past you would not see many people buying houses, but now there are a lot of enquiries from professionals looking for mortgages.

TI: You are Zimbabwean. How would you define the investment framework in Tanzania?

IC: Tanzania offers quite a lot in terms of attractions for investment. Particularly the government is very keen to grow the commercial agriculture and to me there is a very great future in this sector in Tanzania.

Also, there is an enabling environment for investment.

I think it is easier to come and open a business here than in many other countries whereby the role played by the Tanzania Investment Centre and the several incentives available are quite pivotal in attracting investment in this country.

At the same time the political climate is very stable whereby a number of elections have been held successfully and peacefully since the independence. {xtypo_quote_right}If one has a very good project and money, this is the country to invest in.{/xtypo_quote_right}

Also the macroeconomic policies of the government are quite consistent and they are encouraging the private sector to take the leading role.

Unfortunately many still associate Tanzania with its socials past and some lose out on opportunities until they come here to understand the situation.

If one has a very good project and money, this is the country to invest in.

Want to know more about Banking in Tanzania? Our free overview of the Tanzania Business and Investment Guide 2026 covers Banking, plus key sectors and investment opportunities. The complete 141-page edition includes policies, taxation, key regulations, full macroeconomic data, and sources.

Download Free OverviewGet the Full Guide