TanzaniaInvest.Com interviewed CEO of International Commercial Bank Tanzania; Baseer Mohammed as he shared profound insight on the banking industry in Tanzania, borrower and lender information and ICB role in the country’s competitive finance sector.

TanzaniaInvest.com : What does Tanzania represent within the group development strategy in the African continent?

Baseer Mohammed : ICB Group operates in Africa, Eastern Europe and Asia. In Asia we have a large bank in Indonesia and Bangladesh. The group is widely spread in most of the countries and East and West Africa.

For ICB Group,Tanzania is one of the key strategic destinations in Africa where ICB has been one of first foreign banks started operations in 1998 as per the vision of our Share holders from Malaysia to participate and contribute for the growth and development of these emerging economies. {xtypo_quote_right}For ICB Groupn Tanzania is one of the key strategic destinations in Africa{/xtypo_quote_right}

TI : What is your view on Tanzania’s banking sector current situation and next evolution?

BM : The banking Industry in Tanzania comprises of 50 banks which can be categorized into large, medium and small banks. We are one of the medium size banks in the country. The core capital ratio to total risk-weighted capital in the industry has been at 17.38% against the present regulatory requirement of 12% as on 31st Dec 2012.

The overall quality of ratio of Non-performing loans to gross loans were at 7.37% as on Dec 2012. In view of strict monitoring by Bank of Tanzania, the banking industry is resilient to any adverse movements to interest rates, exchange rates and credit quality and protected against any liquidity risk.

Technology is going to drive the efficiencies for the Banks. The introduction of digital clearance system is going to cut the risks of errors saves considerable time and cost to the banks. The system enables encryption and transmissions of images and data files from participating banks to Automated clearing house.

With the kick-off of the credit reference bureau, the access to the borrower information would become easier. This helps in increasing the trust and transparency between lenders and borrowers and improves the quality of credit.

With competition becoming intense there is scope for consolidation in the industry with the increasing interest in takeovers/ mergers etc.

TI: What would you say makes Tanzania unique compared to other African countries?

BM : I see a lot of vibrance in the economy. Vibrance in terms of business, the action and business response. The execution of business is very fast here. As a bank and quality of sales for a bank, it is very good.

Tanzania also has a very strong Asian and Chinese business community compared to other African countries. The people act quite fast here, the execution is very quick. In terms of productivity, Tanzania is very good.

TI: As you say, it is very fast at the same time Banking in Tanzania is very competitive. There are 50 financial institutions here. How do you insure your success and position as a bank in Tanzania?

BM : If you look at the top 3 banks, they have taken about 48% of the market share. We have a market access of 19% so we fall under a medium bank. I would position myself as a medium bank.

The small and medium banks have huge potential for business. {xtypo_quote_left}The small and medium banks have huge potential for business.{/xtypo_quote_left}.

TI : Which segments of banking do you think are still unexploited?

BM : SMEs is one of the segments. Our focus is on SME and Corporate Banking. We are a niche bank. SME is still the unexploited market in Tanzania, that is the huge potential.

TI : Where do you see the most interesting investment opportunities in Tanzania?

BM : Agriculture is always an available opportunity for investment in Tanzania. The Chinese are dominating other infrastructure.

{xtypo_quote_right}Power and transportation are good investments in Tanzania.{/xtypo_quote_right}

There is room for other investors, for hydropower and so forth. Power and transportation are good investments in Tanzania.

TI : With 50 banks and financial institutions and a total population of 45 million, competition is intense in Tanzanian banking sector.

BM : With more players in the Banking industry the products and offerings are going to be finer and precise to meet the specific needs of the customers. The Banks would be compelled to deliver better quality products and services.

There is still a huge opportunity for business growth for the small and medium banks with top 3banks still taking 48% of market share primarily due to their large network and vintage. With the agency banking being introduced the operating models of enrolment and servicing the clients would also undergo a transformation.

TI : What is your bank’s current positioning and core business in Tanzania?

BM : Currently, we have 4 branches; we are opening another branch at Vijena shortly. We would like to consolidate the business and improve the profitability in the existing branches and plan for upcountry expansion in Mwanza, Arusha locations in the second half of this year.

Our core business is funding to corporate/SME customers, Trade finance, Foreign exchange and remittances.

TI : What are your competitive advantages?

BM : In view of the presence of our banks in different countries, we carry the expertise of understanding the clients from diverse industries and different operating environments.

We have a Board with professionals with comprehensive exposure in multinational banks in different geographies. This expertise helps us in understanding the various business models of the customers and structuring the products to tailor their needs.

This specialization is highly essential for large customers who are our focused clientele.

TI : What are your objectives in terms of business development?

BM : We would continue to be a niche player in the market with focus on corporate/ large SME customers and selectively in consumer banking business. During the last financial we had demonstrated a 44% growth on total Assets. Around 85% of the incremental growth in loan book is targeted from SME/ Corporate Customers and 15% from Consumer banking segments.

We are engaging with the Government (TRA) to facilitate collection of taxes etc. We would be increasing our deposit base primarily through increasing the number of accounts from Business and Savings customers.

TI : What are the challenges ahead?

BM : The key challenge is managing the Non Performing loans (NPLs). The legal system is slow and the process of sale and realization of amounts financed is quite cumbersome. This affects the portfolio of banks due to increase in provisioning costs.

The interest rate scenario continues to be very high. Interest rates on loans in shillings are anywhere between 18 to 24 % .This increases the cost of borrowing which fuels the inflation and holds the economic growth.

The rates of interest are high due to the risks involved in the exposures as well is the function of instruments operating in the market.

TI : Mobile money, initiated in Kenya is experiencing incredible popularity in Tanzania. How is this influencing your development strategy?

BM :Mobile money has already revolutionized the payment and settlement system and the value of transactions are projected to be US$ 200 Million by 2015, which is around 8% of nominal GDP of Africa.

{xtypo_quote_left}Mobile money has already revolutionized the payment and settlement system and the value of transactions are projected to be US$ 200 Million by 2015, which is around 8% of nominal GDP of Africa.{/xtypo_quote_left}

This is going to transform the entire mobile eco system and lead to convergence in the payments and solutions with banking payment systems. This is going to integrate the movement of funds from bankable to non- bankable population seamlessly.

As the customer base of the bank increases, we will work out strategic alliances with the partners based on the emerging scenario in the Mobile money eco system.

TI : Which new products and services do you plan to introduce in this market?

BM : We are working out strategic tie-ups with Bank of China which would facilitate trade transactions between Chinese customers who drive the major construction and infrastructure sectors here.

On the consumer banking side, we have launched Mortgage product and would finance projects selectively. We are engaging with various large Car dealers for strategic arrangements on launching Auto loan products. In view of emerging middle class segment the demand for these products is increasing.

TI : The Tanzanian economy is expected to maintain its strong growth, combined with increasing FDI, also thanks to the uprising oil & gas industry, On which sectors do you have the greatest expectations?

BM : The World Bank projected a positive economic outlook over the period 2012-2014. The Tanzanian GDP has been growing consistently and currently recorded 6.5% in 2012. The drivers of growth have been the agriculture, manufacturing, trade, transport and communication sectors.

With the discovery of natural gas, Tanzania being one of the biggest East African markets is expected to play a significant role in the energy sector in the region.

{xtypo_quote_right}With the discovery of natural gas, Tanzania being one of the biggest East African markets is expected to play a significant role in the energy sector in the region.{/xtypo_quote_right}

The maiden visit of President of China to Tanzania signifies the strong ties and the growing interest in Africa. This is leading to large scale investments and trade and development particularly in infrastructure and developmental projects in Tanzania.

TI: What role do you aim to play within this framework?

BM : We would continue to support the companies engaged in manufacturing, infrastructure, trade and transport sectors.

TI : How would you describe Tanzania’s social-economic framework to Investors?

BM : {xtypo_quote_left}Tanzania is a vibrant economy and there are huge opportunities in Agriculture, mining, tourism and manufacturing, infrastructure sectors. {/xtypo_quote_left}

Tanzania is a vibrant economy and there are huge opportunities in Agriculture, mining, tourism and manufacturing, infrastructure sectors. The country has demonstrated strong macroeconomic fundamentals and consistent growth rate, sustainable inflation and implemented various economic and political reforms.

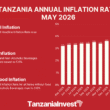

The inflation has been brought down to single digit (9.8%) recently. There a stable political and administrative system that encourages private sector lead growth in the economy.

Want to know more about Banking in Tanzania? Our free overview of the Tanzania Business and Investment Guide 2026 covers Banking, plus key sectors and investment opportunities. The complete 141-page edition includes policies, taxation, key regulations, full macroeconomic data, and sources.

Download Free OverviewGet the Full Guide