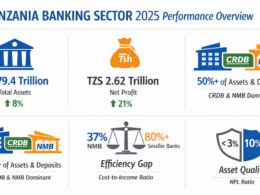

Tanzania Banking Sector Outlook

TANZANIAINVEST has been interviewing Mr. Heri Bomani, former Managing Director of the Kenya Commercial Bank (KCB) Tanzania, to gather his vision and opinion about the country economic outlook and about its banking sector.

| Heri Bomani, Managing Director of the Kenya Commercial Bank Tanzania |

TI: In view of your experience in banking in Tanzania, what do you think is the capacity and willingness of the banks to lend to the sectors that have been identified as key in the economic growth of Tanzania, namely the Small & Medium Enterprises (SME’s) and the agricultural sector?

HB: I have been in the banking sector for 11 years now.

I have had a chance to understand both the corporate side of the business and also the retail side of the banking.

In terms of the agricultural sector, and the Small & Medium Enterprises (SME’s), these are the two key growth areas as identified by the Tanzanian government.

In the case of agriculture, this is the largest sector in the economy.

SME’s are seen as the emerging sector in which the Tanzanians can engage in and participate actively in the growth of the economy.

As for what the banks do for these sectors, I think there has been historical reluctance to participate actively in agriculture.

So clearly it is a sector that has been thought to be very risky; the weather factor has been an issue.

Most of the agriculture is in the remote parts of the country and in terms of physical ability to reach, service and understand the activities on the ground many of the banks have not had direct participation on the activities.

That has also been a barrier. I think what we are now starting to see is that a number of banks are becoming more adventurous.

TI: It seems now though that banks have decided to take more risk in this sense. Why?

HB: There is an obligation to participate in the economic development of the country and agriculture is the backbone of the economy.

Furthermore, a number of banks in Tanzania have realized there are greater opportunities than just investing in government papers.

Banks are taking the view that a certain part of their portfolio can be directed towards agriculture.

Clearly the banks that are best placed for this are the banks with a large distribution network.

They have got the ability to reach these communities, and they have been quite active.

However, there are opportunities for other banks to also provide alternate products and services that add value to the agricultural sector.

This is what we will attempt to do in KCB.

TI: In 2005 the government introduced government credit guarantee schemes to foster banks lending to the abovementioned sectors, particularly SME’s. Is KCB participating in such schemes?

HB: KCB’s objective is to become more participative within the banking sector.

There have been changes made both at the management level as well as at the board level.

Our focus now is to become a more active player in the economy.

Specifically, the credit guarantee scheme is a great initiative by the government and KCB will look to participate actively in such initiatives going forward.

TI: Are SME’s with sound business plans or business track records currently being able to obtain funding without providing any collateral?

HB: The credit guarantee scheme is a good initiative, though it does not completely address all the problems of the SME’s.

{xtypo_quote_right}The challenge for the banks is to look more closely at this segment and understand what are their needs.{/xtypo_quote_right}The challenge for the banks is to look more closely at this segment and understand what are their needs.

Most SME’s operate very informally. If you look at their activities, they do not organize themselves in a way that the banks will understand what their businesses operations are, and whether they are profitable.

On the issue of collateral again, many are start up companies and do not have a history of borrowing, or have property which they can make readily available to banks.

The business owners invest equity to the business, thereby taking the risk to start up the company.

They then look to the banks to come on board and lend against the floating assets and stocks. Most banks are to take on this kind of risk.

KCB will look at introducing products that break the barrier in terms of conventional practices that we have witnessed in Tanzania.

TI: KCB is a Kenyan bank that has expanded regionally into Sudan and Tanzania. Why Tanzania? More in general what is KCB’s international development strategy? Why not Uganda for example?

HB: We have been in Tanzania since 1997, and this is the first international subsidiary bank that KCB established.

Recently, in the last year, the Bank has strategically agreed to embark on regional expansion.

For KCB Tanzania there were some challenges in understanding the needs of the economy and the community, and in getting the right management structure in place.

The bank has addressed these challenges and is now poised for growth.

We take Uganda very seriously and the plan is to quickly establish operation there.

Clearly if you are looking at the Tanzanian market in the context of the East Africa region this is a market that has done exceptionally well.

Uganda has had high rates of growth in the 1990’s and into this century but within the past 5 years Tanzania has come to fore.

So the investment that was made here was opportune, and what is now needed is to leverage and grow the investment in Tanzania, whilst further expanding in the region.

As far as regional expansion is concerned we are in the southern part of Sudan in Juba and we want to play a role in rebuilding that economy.

KCB is the first foreign bank to go to Sudan and set up such an operation. With the regional strategy having been agreed by the board in Kenya I think we will participate actively either by way of acquisition or organic growth in all the markets within the East Africa segment.

We will be looking to expand into Uganda and Rwanda in the medium term.

TI: What do you think makes the Tanzania banking sector so dynamic, with 28 banks that have been able to find their respective niche market?

HB: You need to review the penetration of deposits in terms of GDP.

If you look at the total deposits in the industry that is about US $2.5 billion which is about 25% of the size of the Tanzanian economy.

Most emerging countries would have a higher ratio of penetration, and {xtypo_quote_right}In Tanzania, we are seeing an explosion in growth of deposits{/xtypo_quote_right} in Tanzania, we are seeing an explosion in growth of deposits as the ratio corrects.

Furthermore, there is a lot of informal trade now being formalised into the banking sector.

Importantly we are also starting to see some affluence emerge within the economy as wage levels rise in real terms.

TI: What is the core market KCB is actually targeting in Tanzania?

HB: At this stage, KCB is trying to establish what are the segments in the economy which are not as well serviced as they should be and we would look to focus on these segments.

In terms of what we are doing immediately, there is a large amount of regional trade that happens within East Africa.

We are very well placed to service that trade. We have the biggest branch network within the East African community with over 130 branches between Kenya, Tanzania and Sudan.

There is a lot of trade between Tanzania and Kenya, and there is a lot of investment into Sudan.

Significant trade flows also exist between Tanzania and Uganda and Rwanda.

All of this gives us a strategic opportunity to tap in and to basically add value to the customers who are migrating within these markets.

So, the first focus for KCB is regional trade.

We will also look at the SME segment.

This is a segment, as I mentioned earlier, that is very misunderstood. It is a segment that is informal.

With our experience in Kenya where KCB has hundreds of thousands customers, many of whom are SME’s, we have a number of products and insight into the needs of this segment which we will look to address and add value into Tanzania.

At the same time, if you look at the Tanzanian economy there is a lot of opportunity to provide services to consumers.

This is why retail banking will be an area of key focus in due course.

TI: Why should an SME or any given individual currently banking with another banking institution turn to KCB for their banking services?

HB: Our focus is to do well in this market by understanding the local dynamics and helping to add value to the local consumers.

The KCB group support and infrastructure is also available to us.

The key thing is to get a direct insight on what the consumers in Tanzania are looking for in terms of products and services.

Understanding these needs, and creating an alternate product service options is going to be our real focus.

Tanzania Economy Outlook

TI: What is the realistic expectation on the economic growth of this country upon which you build your development strategy?

HB: Tanzania is a great country.

The country is the biggest in landmark in the region, and its economy has performed well.

From the government right through to the man on the street, there is now a genuine desire to move forward.

Significant infrastructure developments being made in roads and other sectors such as water services.

{xtypo_quote_right}The country is going to be poised for faster growth. The key thing that will make a difference in this country is the people.{/xtypo_quote_right}The country is going to be poised for faster growth.

The key thing that will make a difference in this country is the people.

There has been over the last few years a telling growth in the level of people with ideas, international exposure, business experience and entrepreneurial instinct. I think this was a missing ingredient if you go back about 10 years in history in Tanzania.

People on the ground have now developed that ambition to create wealth, grow and succeed, and to make a difference.

I think this kind of drive in people is what is going to create serious growth in the country.

It is no longer just about what the government is doing for this community; it is also about people themselves starting to embrace the climate of change and having a desire to grow.

TI: What would be your personal piece of advise on Tanzania to our readers?

HB: Often the best experience is a personal experience and what I would recommend to any one thinking of coming to invest here is to make a trip and talk to the stakeholders on the ground so as to have a first hand feel for the economy.

‘Karibuni Tanzania, Karibuni East Africa, Karibuni KCB.’

Want to know more about Banking in Tanzania? Our free overview of the Tanzania Business and Investment Guide 2026 covers Banking, plus key sectors and investment opportunities. The complete 141-page edition includes policies, taxation, key regulations, full macroeconomic data, and sources.

Download Free OverviewGet the Full Guide