Mortgages

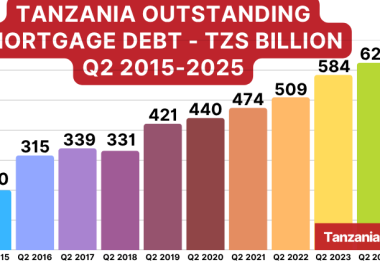

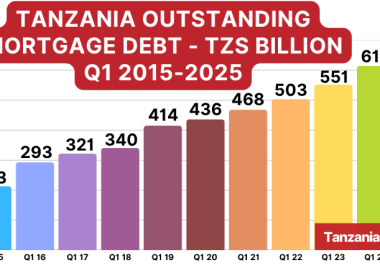

The outstanding mortgage debt as of 30th June 2022 increased to TZS 509.99 billion equivalent to USD 220.23 million.

This is a growth of +7.5% growth in the value of mortgage loans compared to 30th June 2021.

The average mortgage debt size in Q2 2022 was TZS 82.56 million equivalent to USD 35,654, marking a slight increase from TZS 81.49 million equivalent to USD 35,276 reported in Q1 2022.

Tanzania's Mortgage Market in 2021

In 2021, the Tanzanian mortgage market registered an annual growth of 7% reaching an outstanding mortgage debt of TZS 496.61 billion equivalent to USD 215.06 million compared to TZS 464.14 billion equivalent to USD 200.93 million in the year ending 31st December 2020.

The average mortgage debt size as of 31st December 2021 was TZS 80.40 million equivalent to USD 34,815 marking a slight increase from TZS 78.56 million (USD 34,010) in the year ending 31st December 2020.

The ratio of outstanding mortgage debt to Gross Domestic Product (GDP) decreased to 0.35% compared to 0.30% recorded in the year ending 31st December 2020.

Tanzania Mortgage Lenders

As of 30th June 2022, 33 different banking institutions were offering mortgage loans.

The mortgage market was dominated by five top lenders, who commanded 65% of the market.

CRDB Bank was the market leader commanding 38.02% of the mortgage market share, followed by Stanbic Bank (8.11%), Azania Bank (7.13%), NMB Bank (6.82%), and NCBA Bank (4.63%).

The typical interest rates offered by mortgage lenders ranged between an average of 15% and 19%.

Total Mortgage Debt Outstanding by Lenders as of 30th June 2022

Tanzania Mortgage Demand and Constraints to Growth

Tanzania's demand for housing loans is extremely high as it is fueled by the local housing demand which is estimated at 200,000 houses annually and a total housing shortage of 3 million houses.

Tanzania's housing fast-growing demand is mainly driven by the strong and sustained economic growth with GDP growth averaging 6-7% over the past decade, the fast-growing Tanzanian population, which is estimated to more than double by 2050, and efforts by the Government in partnership with global non-profit institutions and foreign Governments to meet the growing demand of affordable housing.

It has also been boosted by easy access to mortgages, with the number of mortgage lenders in the market increasing from 3 in 2009 to 33 by December, and the average mortgage interest rate falling from 22% to 15%.

However, further growth is constrained by an inadequate supply of equitable houses, and high interest rates charged on housing loans.

While interests on mortgage loans improved to 15–19% currently, these interest rates are still relatively high hence negatively affecting affordability.

Also, most lenders offer loans for home purchase and equity release while a few offer loans for self-construction which continue to be expensive and beyond the reach of the average Tanzanians.

Additionally, cumbersome processes around the issuance of titles (especially unit titles) continue to pose a challenge by affecting borrowers’ eligibility to access mortgage loans.

Initiatives to Boost Tanzania's Mortgage Market

The National Housing Corporation (NHC), the Government's company established to undertake an array of business in real estate, has continued carrying out its various projects focusing on high, medium, and low-income earners which continue to have a positive impact on the mortgage market.

Similarly, Watumishi Housing Company (WHC), a public sector property developer continues with the implementation of the Public Servants Housing Scheme, carrying out its various projects focusing on medium and low-income earners and continues to have a positive impact on the mortgage market.

In addition, a key element in the growth of the mortgage market in Tanzania continues to be the provision of long-term funding both in the forms of refinancing and pre-financing by the Tanzania Mortgage Refinance Company (TMRC).

Owned by banks, TMRC was established in 2010 with the sole purpose of supporting banks to do mortgage lending by refinancing banks’ mortgage portfolios, and facilitating Primary Mortgage Lenders (PMLs) in matching their assets (mortgage) and liabilities (funding).

Last Updated: 8th September 2022

Sources: Bank of Tanzania (BoT), Centre for Affordable Housing Finance in Africa (CAHF), Tanzania Mortgage Refinance Company (TMRC).

Want to know more about Mortgages in Tanzania? Our free overview of the Tanzania Business and Investment Guide 2026 covers Mortgages, plus key sectors and investment opportunities. The complete 141-page edition includes policies, taxation, key regulations, full macroeconomic data, and sources.

Download Free OverviewGet the Full Guide