The Bank of Tanzania (BOT) held its Monetary Policy Committee (MPC) on 30th January 2023 to assess the implementation of monetary policy and the performance of the economy, and based on this, decided on the course of monetary policy in the subsequent period.

The MPC noted that the implementation of monetary policy in November and December 2022 was successful. Liquidity in banks was maintained at adequate levels, private sector credit growth was high at around 21%, and monetary targets set forth under the Extended Credit Facility (ECF) were achieved.

The high credit to the private sector is expected to have a significant contribution to the growth of the economy in the fourth quarter of 2022.

In respect of the recent performance of the economy, the MPC observed that global economic challenges continued to undermine activities and exert pressures on inflation in the country, but to a lesser extent than before as the year rolled out.

This was due to the easing of supply-chain disruptions and commodity prices in the world market, as well as interventions made by countries to cushion economies from the adverse impact of the war in Ukraine and the COVID-19 pandemic.

Specifically, the MPC noted that:

i. the economy in Mainland Tanzania and Zanzibar performed satisfactorily in the first three quarters of 2022. In Mainland Tanzania, growth averaged 5.2% compared with 4.8% in the similar period in 2021, driven by agriculture, construction, and manufacturing activities. In Zanzibar, growth was 5.3% compared with 5.8%, mostly contributed by accommodation and food services, construction, manufacturing, and real estate. Based on this performance and economic indicators in quarter four, the MPC was optimistic that growth projections for 2022 will be realized. In 2023, output growth is projected to be higher than in the preceding year, reinforced by strong growth of credit to the private sector, public investment, rebound in tourism, improvement in the business climate, and supportive fiscal and monetary policies. The apparently easing of global supply-chain constraints will also provide impetus to growth;

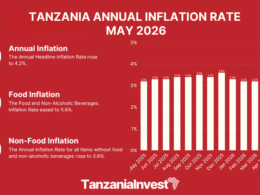

ii. inflation trended upward, largely due to high import prices of consumer goods. However, the pace of increase was comparatively moderate. In Mainland Tanzania, inflation reached 4.9% in November 2022 and eased to 4.8% in the subsequent month. The inflation rate was below the target of 5.4% for 2022/23 and consistent with EAC and SADC convergence criteria of at most 8% and 3-7%, respectively. In Zanzibar, inflation was 7.8% and 8.1% in November and December 2022, compared with the target of 5 %. The MPC observed that, in both economies, inflation was lower than in most of the countries in EAC and SADC, due to interventions made by the Governments to lessen the impact of high prices of imported consumer goods and increase households’ consumption of non-tradable goods. In the outer period, inflation is forecast to remain low and stable, due to the easing of supply constraints and expected good food harvests;

iii. growth of the money supply was broadly in line with the target. Money supply (M3) grew by 11.6% in December 2022, consistent with the target of 10.3 % for 2022/23, and was mostly driven by private sector credit growth. The pace of growth of M3 was also consistent with the inflation target of 5.4%.

iv. government revenue performance was on track in the first half of 2022/23. Domestic revenue performance was strong in Mainland Tanzania and Zanzibar, at 96.7 and 97.1% of the target, respectively. This is attributable to improved tax administration and compliance by taxpayers. Government expenditure was on track, consistent with the need to close the infrastructure gap and cushion the economy from the adverse effects of global shocks;

v. the external sector remained sustainable, albeit weakened by the global shocks, which led to a widening of the current account deficit. Despite the widening of the current account deficit, foreign reserves remained adequate at about 5.2 billion at the end of December 2022, sufficient to cover 4.7 months of imports. The import cover was in line with the country benchmark and EAC convergence criteria of at least 4 and 4.5 months, respectively. The MPC observed that the current account balance and import cover are expected to improve, as import prices in the world market decline.

vi. the banking sector was adequately capitalized, liquid, profitable, and remained resilient to shocks. Assets and deposits of banks continued to increase, supported by the improving business environment, as well as the response to leveraging technology in business and financial services delivery, including the agent banking model. The ratio of non-performing loans continued to decline reaching 5.8% in December 2022, down from 8.5% in the corresponding period in 2021. The MPC noted with satisfaction that, this is a significant milestone compared to the highs of around 13% in 2017. This development will incentivize lending to the private sector and reduce the cost of borrowing.

On the basis of the recent economic performance and outlook for the second half of 2022/23, the MPC decided for the Bank to continue implementing a less accommodative monetary policy stance in January and February 2023.

The policy stance aims at controlling inflationary pressures while safeguarding the growth of economic activities. The policy stance is also consistent with the Bank of Tanzania’s strategies for achieving monetary policy targets set forth under the IMF Extended Credit Facility (ECF) program.

The MPC is optimistic that, with inflation staying below the target of 5.4%, the monetary policy will facilitate high growth in private-sector credit, thereby improving output performances.

Want to know more about the Economy in Tanzania? Our free overview of the Tanzania Business and Investment Guide 2026 covers the Economy, plus key sectors and investment opportunities. The complete 141-page edition includes policies, taxation, key regulations, full macroeconomic data, and sources.

Download Free OverviewGet the Full Guide