TanzaniaInvest interviewed Ravneet Chowdhury CEO of Diamond Trust Bank (DTB) Tanzania, a fast-growing commercial bank focused on SMEs and corporate clients, with a regional presence in Kenya, Uganda, and Burundi.

Chowdhury comments on the improving business environment and crowded banking sector, highlighting shortcomings and potential for credit growth, and DTS’s ambitions and strategy to become one of the top 5 lenders in Tanzania.

You joined DTB Tanzania one year ago, after a long experience in banking in Asia, the Middle East, and Africa. What is your feedback on the business environment in Tanzania so far? Do you perceive tangible improvements since the new administration of President Samia Suluhu Hassan?

We see the business environment in Tanzania as very positive. A lot of effort is being made to smoothen out processes and to attract foreign capital.

A lot of effort is being made to smoothen out processes and to attract foreign capital.

We will however need to do more to ensure that Tanzania captures a fair share of global capital for Investment.

Investors are looking for clarity and stability in rules, an efficient and enabling operating environment that works with speed and minimal bureaucracy.

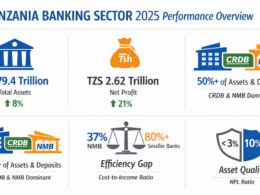

Tanzanian largest banks experienced improvements in profitability in 2021. DTB cumulative net income after tax has reached TZS 8.4 billion in Q3 2021, against TZS 8 billion for the whole of 2020. What are the drivers of these positive performances? What do you expect from now onward?

DTB has indeed seen an improved performance for 2021. This is due to an improving business climate and some recovery from the initial Covid shock.

We have also continued to invest in our digital platforms to provide more convenience to customers.

We have an excellent team that is very energized and is a key competitive advantage for us.

We are focusing on operational efficiency and process improvements to ensure that we continue to provide superior customer service.

We are focusing on operational efficiency and process improvements to ensure that we continue to provide superior customer service.

Access to credit remains a challenge for Tanzanian businesses and individuals, with interest rates averaging 16% and NPLs affecting many banks thus keeping the credit risk high. What does it take to unlock credit to Tanzania’s productive sectors? Which improvements are needed from the regulatory point of view, and what is DTB’s strategy in this regard?

It is important to mention that interest rates have seen a good reduction in the last two years and we continue to see pressure to the downside.

Banks are in the business of lending and we all look for viable projects to lend to whether they are small-scale SME businesses or large corporates.

From a regulatory point of view, we would look forward to a legal system that allows us quick relief and the ability to enforce our rights.

We would look forward to a legal system that allows us quick relief and the ability to enforce our rights.

Our strategy is to continue to support good businesses in the SME and corporate segments and we are committed to playing our part in the growth of the Tanzanian economy.

The Tanzanian market is crowded with 48 licensed banks, though the number is decreasing with the late mergers. Do you foresee further consolidation on new players entering the market? What are DTB’s core markets and competitive advantages and what new markets or initiatives are you pursuing?

Given the size of our economy and the banking revenue pool, we do seem to have many banks in Tanzania.

Further consolidation is inevitable and we see banks merging and possibly some newer players entering the market.

Further consolidation is inevitable and we see banks merging and possibly some newer players entering the market.

DTB Is an East Africa-focused bank with operations in Kenya, Tanzania, Uganda, and Burundi.

We have a competitive advantage in that we are a strong bank with a very clean reputation.

We would like to use our regional presence to provide a more regional solution to our key clients.

For now, we would like to deepen our presence in our existing markets and become more relevant in each one of them.

Enhancing the customer experience through technology, digitization, and innovative product offerings would be our core focus.

In October 2021, President Samia launched the Government’s Economic Recovery Plan worth TZS 3.62 trillion, and the IMF has reviewed upwards its economic forecast for Tanzania for 2022 and 2023. What are your ambitions in terms of growth and what are the main challenges? Which role do you aim to play in the socio-economic development of Tanzania?

We are a top 10 bank in Tanzania today and have an ambition in becoming a top 5 bank.

The key driver for this would be economic growth and stability in policy.

Along with that, we need to become more efficient, digitize our processes and continue to deliver superior services, and provide good value to our customers.

We are a top 10 bank in Tanzania today and have an ambition in becoming a top 5 bank.

DTB is primarily an SME and a Corporate Bank. We also bank individual customers across the country.

Through lending to small customers and large corporates, we play a significant role in the socio-economic development of Tanzania.

We also help facilitate transactions for our retail customers especially through our mobile app.

There is a move to also help with financial inclusion through a digital lending offering.

We are also active in CSR and fund a number of projects in schools and in our local communities.

Want to know more about Banking in Tanzania? Our free overview of the Tanzania Business and Investment Guide 2026 covers Banking, plus key sectors and investment opportunities. The complete 141-page edition includes policies, taxation, key regulations, full macroeconomic data, and sources.

Download Free OverviewGet the Full Guide