Taxation in Tanzania: Guide to The Tax System and Rates

This article provides a comprehensive overview of Tanzania's taxation system, outlining key aspects such as laws and liabilities, tax rates, tax incentives, taxation of expatriates, transfer pricing regulations, VAT, WHT, and more.

Disclaimer The information provided on this page is for general informational purposes only and does not constitute tax, legal, or professional advice. Tax laws, regulations, rates, and administrative practices are complex and subject to change and may vary depending on individual circumstances and interpretation by tax authorities. While reasonable efforts are made to ensure accuracy, TanzaniaInvest makes no representations or warranties regarding the completeness or applicability of the information. Readers are advised to seek independent advice from qualified tax professionals, legal advisors, or the Tanzania Revenue Authority before making any tax-related decisions. TanzaniaInvest accepts no liability for any loss or damage arising from reliance on this information.

Introduction to Tanzania’s Tax System

The Tax Administration Framework

The administration of taxes is governed by the Tax Administration Act, 2015 (TAA, 2015) and tax administration regulations, including the Tax Administration (General) Regulations, 2016.

The Tanzania Revenue Authority (TRA) is the government agency responsible for the administration and collection of taxes in Tanzania. Tanzania has a “self-assessment” tax system in place where the taxpayer is responsible for ensuring compliance with tax laws and regulations by properly presenting tax returns and paying correct taxes.

The TAA, 2015, recognizes approved tax consultants to assist/ represent the taxpayer in tax-related matters. An approved tax consultant is one who has been issued a certificate of registration and approval by the Commissioner General.

The revenue authority has powers to audit the tax affairs of a person before the lapse of five years, with exceptions where there is an indication of fraud that would call for an investigation.

Tax Residency in Tanzania and Tax Liability

In Tanzania, tax liability is determined by residency status. Residents are taxed on their worldwide income, while non-residents are only taxed on their Tanzanian-sourced income.

An individual is a resident in Tanzania if he/she meets any of the following:

(a) has a permanent home in the United Republic of Tanzania and is present in the United Republic of Tanzania during any part of the year of income;

(b) is present in the United Republic of Tanzania during the year of income for a period or periods amounting in aggregate to 183 days or more;

(c) is present in the United Republic of Tanzania during the year of income and in each of the two preceding years of income for periods averaging more than 122 days in each such year of income; or

(d) is an employee or an official of the Government of the United Republic of Tanzania posted abroad during the year of income.

A corporation is a resident corporation for a year of income if:

(a) it is incorporated or formed under the laws of the United Republic of Tanzania; or

(b) at any time during the year of income the management and control of the affairs of the corporation are exercised in the United Republic of Tanzania whether physically or through any electronic means which includes virtual means.

A partnership is a resident partnership for a year of income if at any time during the year of income a partner is a resident of the United Republic of Tanzania.

A trust is a resident trust for a year of income if:

(a) it was established in the United Republic of Tanzania;

(b) at any time during the year of income, a trustee of the trust is a resident person; or

(c) at any time during the year of income a resident person directs or may direct senior managerial decisions of the trust, whether the direction is or may be made alone or jointly with other persons or directly or through one or more interposed entities.

Types of Taxes in Tanzania

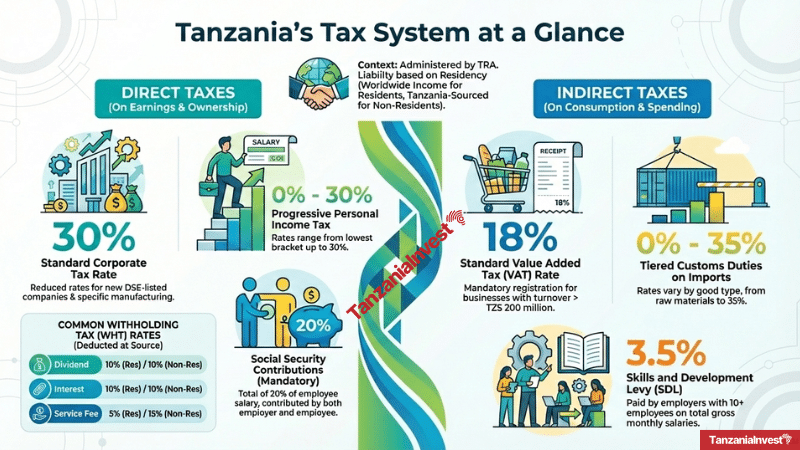

The applicable taxes in Tanzania can be categorized into two broad categories: Direct taxes and Indirect taxes. Direct taxes refer to taxes on what you earn and what you own, while indirect taxes refer to what you spend.

Direct Taxes

Direct taxes are governed by the Income Tax Act, 2004 (ITA,2004) and the supporting regulations, which impose income tax on earnings by a person (individual or entity) from employment, business, and investments where taxes are charged either progressively or at a flat rate.

The laws and regulations cover a range of taxes on earnings particularly employment tax, corporate tax, presumptive tax, single instalment taxes, and withholding taxes.

Tanzania Tax Base (Taxable Income)

Taxable income in Tanzania is grouped into:

Employment income (salaries, wages, bonuses, allowances, and fringe benefits)

Business income (profit and gains from a trade, profession or vocation)

Investment income (dividend, rent, royalty and so forth)

Employment Income Tax in Tanzania

A progressive taxation system applies to resident individuals’ income from employment on amounts below TZS 12,000,000 (annual), and a flat 30% on any excess. The employer is required to withhold such income tax when making payments to an employee and submit a monthly statement indicating, among other information, the names of employees, total employment income per employee, and income tax withheld per employee. Employees do not file tax returns.

Tanzania Personal Income Tax Rates

Total income per annum (TZS)

Tax rate

0 to 3,240,000

NIL

3,240,001 to 6,240,000

8% of the amount exceeding 3,240,000

6,240,001 to 9,120,000

240,000 plus 20% of the amount exceeding 6,240,000

9,120,001 to 12,000,000

816,000 plus 25% of the amount exceeding 9,120,000

Above 12,000,000

1,536,000 plus 30% of the amount exceeding 12,000,000

*Taxable income is exclusive of the employee’s deduction to the social security fund.

Social Security Contributions

In Tanzania, both employees and employers are required to make social security contributions. There are two main social security schemes:

National Social Security Fund (NSSF) for the private sector

Public Service Social Security Fund (PSSSF) for employees of public service.

In both schemes, a total of 20% per employee must be contributed. In NSSF both employees and employers contribute 10% each while for PSSSF employees contribute 5% and employers 15%. These contributions provide benefits such as pensions, disability coverage, and survivors' benefits.

Business and Investment Income Tax in Tanzania

The income tax of an individual is taxed at similar progressive tax rates as those of employment income. Where the total income of a resident individual includes net gains from the realization of certain identified assets, a progressive tax rate applies on the amount exclusive of the net gain. The net gain would be taxed at 10%.

The income of non-resident individuals and of persons from conducting mining and/or petroleum operations is taxed at 30%. An exception is for resident individuals with a business turnover with source in the United Republic of Tanzania not exceeding TZS 100,000,000 per annum, where a presumptive tax regime would apply.

Presumptive taxes are progressive and vary between businesses maintaining documents and those that don’t, the latter attracting slightly higher taxes. A presumptive tax regime does not apply any tax on the turnover not exceeding TZS 4,000,000; taxes 3.5% of turnover above TZS 11,000,000 but not exceeding TZS 100,000,000, and is progressive for the turnover thresholds in between TZS 4,000,000 and TZS 11,000,000. It is more favourable for businesses that are profit-making and in circumstances where maintaining documents is a challenge.

The presumptive income tax regime does not apply to individuals engaged in professional, technical, management, construction, and training services.

Tanzania Corporate Tax

Income tax of a corporation, including limited companies, trusts, unapproved retirement funds, a domestic permanent establishment of a non-resident person, clubs, and trade associations, is taxed at 30%. Income from clubs and trade associations is generally exempt if at least 75% of it is derived from members. Businesses engaged in gaming activities are taxed separately as governed by the Gaming Act.

Lower corporate tax rates apply to special-mentioned types of corporations, including those newly listed at the Dar es Salaam Stock Exchange with at least 30% of their equity ownership issued to the public. For corporations with perpetual unrelieved loss for three consecutive years, an alternative minimum tax shall apply, equivalent to 1% of the turnover of the third year of perpetual unrelieved loss. An exception to this law is corporations conducting agricultural business or engaged in the provision of health or education.

Tanzania Corporate Tax Rates

Entity Description

Rate

Income of a resident corporation

30%

Income of a PE of a non-resident corporation

30%

Income of companies newly listed on the Dar es Salaam Stock Exchange (DSE)

25% for three consecutive years

Income of new assemblers of vehicles, tractors, and fishing boats

10% for the first five years from operations commencement

Income of new manufacturers of pharmaceutical or leather products having performance agreements with Tanzania’s government

20% for the first five years from operations commencement

Companies with perpetual unrelieved tax losses for three consecutive years including the year of income

(Alternative Minimum Tax - AMT)

1% of turnover

Thin Capitalization

The Finance Act 2025 reinstated "retained earnings" in the definition of equity for thin capitalization purposes. The definition now includes positive retained earnings and reads: “equity means paid up share capital and positive retained earnings at the end of the year of income”. This amendment is significant because the removal of retained earnings in a previous definition had disallowed interest cost for some taxpayers.

Additional Taxes

Tanzania Digital Services Tax. This is a single installment tax on non-residents providing digital services for a payment that has a source in Tanzania, at a rate of 2% of gross payments.

Transportation Advance Tax. This is an advance tax on earnings by a resident individual or entity engaged in the transportation of passengers or goods. This tax is based on the number of passengers or load capacity.

Category of vehicle (Class D: Private Hire Service Vehicles)

Tax payable (TZS)

1

Taxi

180,000

2

Ride Hailing

350,000

3

Ride Sharing

450,000

4

Special hire

750,000

Single Instalment Taxes in Tanzania

Tax on what you own provides for a single instalment tax on the gain from the realization of certain assets. The ITA, 2004 provides for a single installment tax on gains in conducting an investment from the realization of an interest in land, petroleum, or mineral rights, or buildings situated in Tanzania, shares or securities held in a resident entity. Single installment tax is also applicable on the sale of forest produce.

The tax rate for single instalment tax is 10% of the gain for a resident person. For a non-resident person, the rate is 30% of the gain from the realization of an interest in land, petroleum, or mineral rights, or buildings situated in Tanzania, shares or securities held in a resident entity. A rate of 30% applies to the realization of mineral rights and/ or petroleum rights. Single instalment tax in relation to the realization of shares, securities, or interest in land is what is also commonly termed as capital gain tax.

For resident persons other than a corporation who harness forest produce for sale, a single instalment tax of 2% of the gross payment is applicable. This is treated as final tax and must be paid before the forest produce is transported. Forest produce includes timber, logs, mirunda, and poles.

Tanzania Withholding Taxes (WHT)

Tax on earnings is also in the form of withholding taxes whereby a tax deduction considered as “withholding tax” is made by a resident person upon making payments. They are advance taxes and may be final or non-final depending on the payment they relate to.

Withholding tax rates in Tanzania differ depending on the nature of the supply and the residence status of the person being paid.

Taxation of retained earnings

The Finance Act 2025 introduces new measures to address the practice of avoiding tax through the non-distribution of dividends. It gives the Commissioner General the authority to collect withholding tax on dividends based on 30% of an entity’s profit if no distribution is made within 12 months after the end of the financial year. The Act clarifies that when dividends are later distributed that were already subject to this deemed withholding tax, there will be no further requirement to withhold income tax on the same amount.

Tanzania Withholding Taxes (WHT) Rates

Tanzania Withholding Taxes (WHT) Rates

Description of Payment

WHT Rate for Resident

WHT Rate for Non-Resident

Dividends from the DSE-listed corporations

5%

5%

Dividend to resident corporations holding at least 25% of the shares and controlling at least 25% of the voting rights in the corporation

5%

10%

Dividends from other corporations

10%

10%

Interest

10%

10%

Royalties*

15%

15%

Rent (construction equipment, land, and buildings)

10%

10%

Aircraft lease

10%

10%

Rent on other assets (other than construction equipment, aircraft, land, or buildings)

N/A

10%

Management or technical services fees for mining, oil, or gas

10%

15%

Insurance Premium

N/A

10%

Natural Resources Payment

15%

15%

Service Fees

5%

15%

Money transfer commission to a money transfer agent

10%

N/A

Fee or any other charge to a commercial bank agent

10%

N/A

Fee or any other charge to a digital content creator

5%

N/A

Payments for goods supplied to the Government and its institutions by any person

2%

N/A

Payments for the purchase of precious metals/gemstones, industrial and metallic minerals

2%

N/A

Verified carbon emission reduction

10%

N/A

Exchange or transfer of digital assets made by a resident person

3%

N/A

Hired motor vehicles (to resident persons)

10%

N/A

Commission for gaming advertisement or promotion payments

10%

N/A

Indirect Taxes

The other important category is the applicable taxes on consumption/ purchase. Indirect taxes in Tanzania include Value Added Tax (VAT), Excise Duty, and Customs Duty.

Tanzania Mainland and Zanzibar have independent VAT laws and regulations. Classes of VAT include taxable and exempt supplies. Taxable supplies include supplies made at a standard rate of 18% and supplies made at a zero rate of 0%. Except as provided, all supplies are regarded as taxable supplies. In most cases, taxable supplies would be charged VAT at a zero rate if supplied or used outside Tanzania. Money is not considered a form of supply.

A reduced rate of 16% applies to supplies made in Mainland Tanzania to an unregistered person, provided the consideration for such supply is made through a bank or electronic payment system approved by the Commissioner General.

VAT registration is mandatory for businesses with an annual turnover exceeding TZS 200 million. Government entities, professional service providers, and certain other entities are also required to register regardless of turnover if they are engaged in taxable economic activities. Once a taxpayer is registered for VAT, they will be required to file a VAT return and pay any tax due by the 20th of every month following that to which it relates. The exception that previously allowed filing on the next working day when the 20th falls on a weekend or public holiday has been abolished. A nil VAT return will be filed where no transactions occurred during the reporting period.

VAT becomes payable when the net effect between VAT on sales is higher than VAT on purchases, and a receivable if the vice-versa occurs.

The Finance Act 2025 introduced VAT withholding agents to improve VAT collection on supplies made to them. These agents include the Ministry of Finance, government entities that retain part of their collected revenue, and any registered person appointed by the Commissioner General of the Tanzania Revenue Authority. They are required to withhold 3% VAT on goods and 6% on services for standard-rated supplies and remit the withheld amounts to the TRA by the filing due date.

Excise Duty in Tanzania

Excise duties are indirect taxes on the sale, use, manufacture, or importation of specific products and services. It is charged in both specific and ad valorem rates. The liability to pay excise duty falls on either the purchaser or the seller, depending on the nature of the item supplied. Unlike most other countries, excise duty also applies to fees charged by financial institutions and telecommunication service providers, pay-to-view television services, and electronic communication services supplied by electronic communication service providers.

The Finance Act 2025 has provided a definition of a financial institution to mean a bank or financial institution licensed under the Bank of Tanzania Act or the Banking and Financial Institutions Act, including Tier 1 microfinance service providers, which are recognized under the Microfinance Act.

The Act has extended dutiable value definition for the purpose of charging excise duty on electronic communication services, to also cover the use of a cable in providing electronic communication services. Initially, this definition only covered the amount payable for electronic communication service supplied in respect of using a mobile phone, whether fixed or wireless.

Excise duty filing of the return and payment of the duty is due on the 25th of the following month to which it relates. A nil excise duty return is filed even where there are no dutiable transactions during the period. The deadline for expiry of an excise duty license is twelve months from the date of issuance of the license.

Increase in excise duty

Introduction of 10% excise duty on the service providers of money transfer and payment systems who employ independent systems other than financial or telecommunication systems.

Introduction of additional excise duty of 20% on imported used tableware, kitchenware, utensils, cutlery, and other related products.

There are also increases in excise duty on various goods and services.

Customs Duties in Tanzania

Custom duties are applicable upon the importation of goods. Favourable rates and rules are applicable upon importation from members of the East African Community (EAC) where rules of Origin criteria are met. Customs duty rates vary depending on the nature of goods.

Customs Duty Ratesin Tanzania

Goods

Rate

Raw materials, agricultural inputs, pharmaceuticals, and medicines

0%

Industrial used goods

10%

Consumer goods

25%

Specified goods

35%

Other Taxes and Levies

Skills and Development Levy (SDL)

SDL is governed by the Vocation Education Training Act and is charged at a rate of 3.5% of the total gross emoluments made by the employer to the employees in the respective month, where the number of employees is ten or above.

Every employer is required to file SDL returns by the 7th day following the month to which SDL relates. Where SDL is payable, the employer should submit payments by the 7th day following the month to which SDL relates.

Tanzania Stamp Duty

While it is applicable to several instruments, the most common one is the lease agreements, where stamp duty would be paid by the lessee at 1% of the annual value of the lease agreement for the duration of the lease, and agreements or memorandum of agreement (exemptions considered) at TZS 500/=.

Other Changes

Airport Service Charge Act

The Finance Act 2025 has amended the due date for payment of port service charges from “last working day” to “20th day” of the month following the month of collection of the charges to align with the date for submitting returns.

Revenue Sources for HIV/AIDS Control and Universal Health Coverage

The Finance Act 2025 has amended various laws to create a domestic revenue source for funding HIV/AIDS control programs and Universal Health coverage. 70% of the new funds will go to the AIDS Trust Fund and 30% to the Universal Health Insurance Fund. Changes made are as follows.

Increase excise duty rate by TZS 10 per litre on beer (under Heading 22.03); TZS 15 per litre on wine and other fermented beverages (under Headings 22.04, 22.05 and 22.06), and TZS 25 per litre on spirits, liquors and other spirituous beverages (under Heading 22.08) (Excise (Management and Tariff) Act;

Introduction of fuel levy of TZS 10 per litre on petrol, diesel and kerosene (Road and Fuel Tolls Act);

Introduction of a levy of 0.1% on the gross market value of minerals (Mining Act);

An increase in winning tax on sports betting from 10% to 12%, and on land-based casinos from 12% to 13% (Gaming Act).

Taxation of Expatriates in Tanzania

Expatriates (aka expats) working in Tanzania are subject to the same personal income tax rates as residents. However, they are taxed only on their Tanzanian-sourced income.

Tax treaties may affect the taxation of expatriates in Tanzania. These agreements help prevent double taxation and often provide for reduced withholding tax rates on certain types of income.

Double Tax Treaties in Place with Tanzania

Tanzania has double tax treaties (DTT) with nine countries which may provide for a lower rate of withholding tax (WHT).

Canada - Tanzania Income and Capital Tax Treaty (1995)

Denmark - Tanzania Income and Capital Tax Treaty (1976)

Finland - Tanzania Income and Capital Tax Treaty (1976)

India - Tanzania Income Tax Treaty (1979)

Italy - Tanzania Income Tax Treaty (1973)

Norway - Tanzania Income and Capital Tax Treaty (1976)

South Africa - Tanzania Income Tax Treaty (2005)

Sweden - Tanzania Income and Capital Tax Treaty (1976)

Zambia - Tanzania Income Tax Treaty (1968)

Tanzania has also signed Double Taxation Agreements with Oman in 2024, the Czech Republic in 2025, and Turkey and Singapore in 2026. However, they are yet to be ratified.

Transfer Pricing is the process of pricing the exchange of goods and services between associates. In Tanzania, an associate is a relative of an individual, a partner in a partnership, an individual or a company that has more than 25% shareholding in another company, or anyone (other than an employee) that may have influence in the company.

Legislative Requirements

Section 33 of the Income Tax Act, 2004 requires transactions between associates to be conducted at arm’s length, i.e., as if conducted between parties that are not related. As a result, the Income Tax (Transfer Pricing) Regulations, 2014, were introduced in February 2014, with a requirement for companies transacting with their associates to prepare and maintain contemporaneous transfer pricing documentation. The document needs to explain the transaction flow, the pricing policies applied, and demonstrate that they are conducted at arm’s length. The 2014 TP Regulations were repealed in April 2018 and replaced with the Tax Administration (Transfer Pricing) Regulations, 2018. The 2018 TP Regulations were more robust and in alignment with the global transfer pricing standards.

Regulation 7 of the TP Regulations requires a transfer pricing document to be in place by the time of filing the final tax return, i.e., 6 months after the financial year-end. If requested by the Tanzania Revenue Authority (TRA), then it should be submitted within 30 days. However, if the total magnitude of the related party transactions during the year is TZS 10 billion (approx. USD 4.27M) and above, then the transfer pricing document needs to be filed with the revenue authority along with the final tax return. An extension of a maximum of up to 30 days can be provided upon request.

The Finance Act 2025 introduced a proviso in section 44(1) concerning assets transferred between associates. The new proviso dictates that where the recipient person subsequently realizes or transfers ownership of the asset, the cost of the asset for purposes of computing gains or losses shall be the net cost of the asset at the time of acquisition of the asset by that other person and subsequent costs after acquisition. This calculation proceeds "as if the person and the other person were the same".

Penalties for Non-Compliance

Failure to comply with Regulation 7 (i.e., maintain or submit documents when due) results in a penalty of TZS 52.5M (approx. USD 22,435) per year. Additionally, failure to comply with the arm’s length principle results in a penalty of 100% of the tax liability resulting from the transfer pricing adjustments. The penalty for failure to conduct related-party transactions at arm’s length is also extended to cover entities in a tax loss position, where the penalty will be 30% of the adjusted loss.

Transfer Pricing Audits

The TRA has a special unit within the Large Taxpayers Department, called the International Taxation Unit (ITU), which comprises officials who are knowledgeable and experienced in transfer pricing. This department is responsible for conducting transfer pricing audits for large taxpayers and provides support to the TRA regional offices in transfer pricing matters during tax audits. In many instances, if taxpayers in other regional offices have a high-risk profile, the TRA auditors from the regional teams request the ITU to conduct a special transfer pricing audit.

Transfer pricing audits are special audits that are either conducted concurrently with general tax audits or separately. Therefore, if the TRA auditors have closed an audit for a particular year, they can reopen the years and review the transfer pricing affairs of the taxpayer. These audits typically begin with the TRA requesting to review the taxpayers’ transfer pricing documents in place, which need to be submitted within 30 days. Failure to do so results in a penalty of TZS 52.5M as mentioned above. Thereafter, interviews are conducted to understand the functions performed, assets utilized, and risks assumed while undertaking transactions. The law provides the taxpayer with 14 days to respond to the audit findings once they are issued. However, a maximum of an additional 14 days may be granted upon request to the Commissioner of the TRA.

Under the Tanzanian Income Tax Act, 2004, there are several tax incentives (Exemptions and Deductions) available:

Reduced Corporate Tax Rate for Listed Companies

There is a reduced corporate rate of 25% which is charged for three years to newly listed companies with the Dar es Salaam Stock Exchange, with at least 35% of equity shares issued to the public.

100% Capital Allowance In Agriculture

Investors in agriculture enjoy 100% capital allowance on expenditure incurred on plant and machinery, including windmills, electric generators, and distribution equipment used solely in agriculture.

50% Initial Capital Allowance

The 50% allowance is granted on the expenditure of plant and machinery that is used in manufacturing and installed in the factory, or providing services to tourists and fixed in a hotel. Other rates for capital allowances range from 37.5% for items like computers and earthmoving equipment to 5% for buildings, dams, water reservoirs, etc.

Withholding Tax Exemption

The law provides an exemption from withholding tax chargeable by foreign banks on interests payable to strategic investors as defined by the Tanzania Investment Act.

Tax Credit

The income tax law of Tanzania provides for a tax credit in case the tax was paid abroad on the same income, which was assessed with respect to a resident person (individual or entity).

Income Tax Exemption Under Export Processing Zone (EPZ)

The following amounts are exempted from income tax:

Income derived from investment or business conducted within the Export Processing Zone and Special Economic Zone, during the initial period of ten years. The Finance Act 2025 specifically restricts this exemption to profits derived from local sales.

Payment of withholding tax with respect to foreign loans granted to investors licensed under the Export Processing Zone and Special Economic Zone during the initial period of ten years.

Payment of withholding tax on dividends arising from investment in the Export Processing Zone and Special Economic Zone during the initial period of ten years.

Payment of withholding tax on the rent payable by an investor licensed under the Export Processing Zone and Special Economic Zone during the initial period of ten years.

Tax Compliance and Filing Requirements

Tax Year

The tax year in Tanzania follows the calendar year, beginning on January 1 and ending on December 31. Tax years not coinciding with the calendar year in relation to income from any source other than employment or services rendered are permitted, subject to approval from the Commissioner. A threshold for certification of tax returns by a Certified Public Accountant (CPA) has been introduced: Individuals with an annual turnover exceeding TZS 500 million and corporations with gross annual income exceeding TZS 100 million are required to have their returns certified.

Tax Returns and Payments

Companies are required to file provisional tax returns and make provisional tax payments quarterly, within three months after the end of each quarter. The final corporate income tax return must be filed within six months following the end of the tax year. Any outstanding tax liability must be settled by the time the final return is submitted. Employment taxes and taxes on digital services are paid on a monthly basis by the 7th of the month following that to which they are related. Single installment taxes are paid within 30 days from the date of realization of an asset.

Certification of Tax Returns

The Finance Act 2025 has introduced a threshold for certification of tax returns by a CPA to relieve small and medium entrepreneurs from compliance costs. The threshold is for individuals with an annual turnover exceeding TZS 500 million and for corporations with gross annual income exceeding TZS 100 million.

Considerations on The Tanzanian Tax Administration Framework

Must One Agree To A Tax Decision?

Where a taxpayer is aggrieved by a tax decision, an objection or appeal is filed in the stipulated manner and time. The person aggrieved by the tax decision has the burden of proof to counter the decision.

Punishments For Tax Non-Compliance

Punishments for non-compliance with tax laws and regulations impose fines, imprisonment, penalties, or interests. Fines and imprisonment sentences vary depending on the nature of the offense. Penalties and Interests, on the other hand, have a fixed factor of the rate or currency points but a variable factor of the time length of non-compliance.

Specifically, TAA, 2015, as amended by the Finance Act, 2024, imposes a penalty for late filing of tax returns or late payment of taxes at the higher of 2.5% of the tax liability and TZS 300,000 (TZS 100,000 for individuals), per month or part of the month. This change reflects the increase in the value of currency points from TZS 15,000 to TZS 20,000 under the Finance Act, 2024. Interest on late payment of tax continues to accrue at a statutory rate per month or part of the month.

Tax Overpayments And Refunds

In cases where a person has made an overpayment of tax, an application should be made by the person to the Commissioner General (CG) to request a refund. Where the CG is satisfied, the excess tax is offset against other taxes, and any remaining excess tax is repaid to the person.

The E-Filing System (Online Tax Return Filing)

TRA's online gateway portal allows taxpayers to manage their tax affairs, including the filing of their tax returns and generating transfer forms to initiate tax payments. A taxpayer can obtain access to e-filing through online self-registration using a person’s tax identification number (TIN).

Taxpayers are required to interface their electronic systems with the electronic system established by the Commissioner upon receipt of a written notice from him. Failure to interface with the electronic system is an offense resulting in fines upon conviction.

Every person who becomes potentially liable to tax by reason of a carrying business, investment, or employment shall apply to the Commissioner General (CG) of the revenue authority for a TIN within fifteen (15) days from the date of commencing the business, investment, or employment, or as the CG may determine. Furthermore, to make sure each required person is registered for tax purposes, the CG has been given the mandate to register and issue a TIN to every Tanzanian citizen who is registered and issued with a National Identification Number (“NIDA”), such that each person’s TIN is connected with their NIDA. A person can only have one TIN.

Fiscal Invoices/ Receipts

Any person supplying goods, rendering services, or receiving payments in respect of goods or services rendered shall issue a fiscal receipt or fiscal invoice unless they are excluded from the requirement. One of the categories of exclusion is for businesses with less than TZS 11,000,000 annual turnover.

The Tanzania Revenue Authority (TRA) has adopted new strategies to reach a revenue collection target of TZS 41.830 trillion for the 2026/2027 financial year. The Authority collected TZS 37.96 trillion in 2025/2026, equivalent to 105% of its TZS 36.07 trillion target.

Tanzania’s Finance Bill 2026, presented to Parliament on 24 June 2026 by Finance Minister Ambassador Khamis Mussa Omar, takes effect on 1 July 2026 and amends 26 laws to implement the 2026/27 budget tax measures. The Parliamentary Budget Committee dropped the proposed 1% withholding tax on agricultural produce, the proposed 5% excise on motorcycles and on gambling stakes, softened excise duties on imported used vehicles, cut the SME presumptive tax to 4.0% from 4.5%, confirmed mining Framework Agreement tax incentives during the construction phase, and introduced a new 0.5% stamp duty on agricultural land transfers.

Tanzania's 2026/27 budget is set at TZS 62.33 trillion (USD 24 billion), up 10.3% from the previous financial year, targeting 6.3% GDP growth with 74.2% financed from domestic revenue as grants fall 39.1%. Key investor measures include halving the deemed profit-distribution tax from 30% to 15%, a one-year income tax holiday for newly registered businesses, retained VAT deferment on imported capital goods, and VAT exemptions across compressed natural gas, electric vehicle charging equipment, and LPG infrastructure.

Tanzania and Singapore signed five agreements and memoranda of understanding during President Tharman Shanmugaratnam’s state visit to Tanzania, covering taxation, trade facilitation, public service capacity building and diplomatic cooperation. The two countries also reaffirmed plans to deepen collaboration in investment, digital transformation, logistics, financial services and industrial development as bilateral trade reached USD 74 million and Singaporean investments in Tanzania exceeded USD 535 million.

Tanzania and Türkiye have signed two Double Taxation Agreements (DTAs) at a ceremony in Dar es Salaam, marking the 13th such treaty for Tanzania and closing a long-standing gap in the bilateral economic framework that already included a 2011 Bilateral Investment Treaty. The agreements support a joint trade and investment roadmap valued at USD 1 billion, building on bilateral trade of USD 281.68 million recorded after President Samia Suluhu Hassan's 2024 visit to Türkiye.

The Presidential Commission has officially submitted a comprehensive report detailing 284 Tanzania tax system reforms to President Samia Suluhu Hassan. The Tanzania Private Sector Federation (TPSF) anticipates these changes will significantly reduce compliance costs and create a highly predictable business environment.

The Tanzania Revenue Authority (TRA) will launch the Integrated Domestic Revenue Administration System (IDRAS) to expand the tax base, curb evasion, and simplify compliance. IDRAS will allow taxpayers to issue electronic fiscal receipts and track applications, while training for tax consultants begins to ensure smooth adoption.

The Ministry of Finance of Tanzania has opened submissions for the 2026/27 Tax Reform Task Force. Stakeholders are invited to propose changes to tax and non-tax policies, analyze sectoral impacts, and recommend measures to achieve fiscal objectives while supporting priority sectors under the Tanzania Development Vision 2050. Submissions are open until 31 March 2026.

Tanzania has launched the Medium Term Revenue Strategy 2025/26–2027/28 to enhance tax compliance, address evasion loopholes, and reduce the budget deficit. The strategy introduces reforms in policy, administration, and laws to strengthen domestic revenue collection and ensure sustainable financing of development projects.

The Tanzania Revenue Authority has set up 200 Trade Facilitation Desks nationwide to identify traders, address business challenges, and support entrepreneurship. The desks, starting operations on August 19, 2025, will also gather feedback to improve the business environment.

August 19, 2025

Want to know more about investing in Tanzania? Our free overview of the Tanzania Business and Investment Guide 2026 covers the economy, key sectors and investment opportunities.

The complete 141-page edition, which includes policies, taxation, key regulations, full macroeconomic data and sources, is also available at no cost upon completion of a short form.

This website uses cookies to improve your experience. By continuing to browse the site, you are agreeing to our use of cookies.Accept

Privacy & Cookies Policy

Privacy Overview

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. This category only includes cookies that ensures basic functionalities and security features of the website. These cookies do not store any personal information.

Any cookies that may not be particularly necessary for the website to function and is used specifically to collect user personal data via analytics, ads, other embedded contents are termed as non-necessary cookies. It is mandatory to procure user consent prior to running these cookies on your website.