Finance

Tanzania's financial sector—spanning Banking, Capital Markets, Insurance, and social security—contributed 3.5% of GDP in the first nine months of 2025 and grew 14.8% year-on-year, with Banking accounting for 70.2% of total financial assets and the Dar es Salaam Stock Exchange reaching a market capitalization of USD 9.42 billion.[1][4]

Tanzania's financial system is structured around four interlinked pillars, with Banking representing 70.2% of total financial assets, followed by social security at 24.1%.[1]

The total assets-to-GDP ratio reached 44.2% in 2024, with collective investment schemes recording the highest growth at 46.1%, followed by Insurance and Banking.[6]

The sector is anchored by the Financial Sector Development Master Plan 2020/21-2029/30, a long-term reform framework providing a unified strategy across Banking, Capital Markets, Insurance, and other financial services.[13]

Underpinning sector expansion is a network of Development Finance Partners—including the AfDB (African Development Bank), the World Bank, the IFC (International Finance Corporation), the IMF, AFD (Agence Française de Développement), the EIB (European Investment Bank), and the AEF—which provide multi-billion-dollar long-term financing and technical assistance across infrastructure, financial inclusion, and private sector growth.

Major flagship interventions backed by these partners include the AfDB-financed USD 272.12 million Msalato International Airport in Dodoma, the World Bank-anchored Tanzania Mortgage Refinance Company under the Housing Finance Project, and IFC co-investments with local Banks across SME and agribusiness finance.

Banking

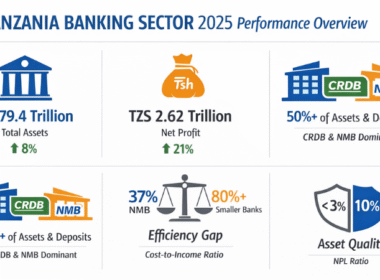

Tanzania's banking industry comprises 44 licensed banking institutions, including 34 commercial Banks (97.3% of total banking sector assets), three community Banks, three microfinance Banks, two development Banks, one house financing company, and one mortgage refinancing company.[7]

Of the 34 commercial Banks, 12 are locally owned and hold 65.7% of commercial bank assets, while 22 are foreign-owned and hold 34.3%.

The sector is highly concentrated—in 2024 the ten largest Banks held 79.4% of total assets, 82.4% of total loans, and 80.4% of total deposits, with the two largest Banks (with significant Government shareholding) jointly accounting for nearly half of all total assets.

Total banking assets reached TZS 62,165.1 billion in 2024 (+14.6%), profit reached TZS 2,129.0 billion (+39.3%), return on assets stood at 5.2%, and return on equity at 23.7%.[8]

The loan portfolio is dominated by personal loans (37.2%), followed by trade (12.5%), agriculture (12.4%), and manufacturing (9.6%); the NPL ratio fell to 3.4% in 2024 and further to 2.8% by December 2025.[3]

Lending rates averaged 16% in 2024 and 15% in 2025, while deposit rates averaged around 8%.

Network expansion continued with 1,028 bank branches in 2024 (up from 1,011) and 145,430 banking agents, while 62,232 licensed microfinance service providers operated at end of 2024 under the Microfinance Act 2018, with Tier 4 Community Microfinance Groups accounting for 94.7%.

Islamic Banking continues to deepen, with Islamic deposits at 3.0% of total banking deposits and Sharia-compliant financing at 2.6% of total industry credit in 2025; the first fully-fledged Islamic bank has been operational since 2011 and several conventional Banks now offer Sharia-compliant products.[1]

Capital Markets

The Dar es Salaam Stock Exchange (DSE) hosts 28 listed companies (22 domestic, six cross-listed) and is regulated by the Capital Markets and Securities Authority (CMSA), established in 1995.

Total market capitalization reached TZS 23,995.45 billion (approximately USD 9.42 billion) in 2025, up 34.30% from 2024, while domestic market cap stood at TZS 15,559.44 billion (USD 6.11 billion), up 27.08%.[11]

The DSE All Share Index (DSEI) rose 29.08% YoY, the Tanzania Share Index (TSI) gained 24.70%, and the Banks/Finance/Investments Index surged 88.46%.

Total equity market turnover reached TZS 663.75 billion in 2025 (+190.31%), with total traded volume of 477.81 million shares (+109.57%); mobile trading via Hisa Kiganjani drove a 656.38% YoY turnover surge and a 316.28% jump in new CDS account registrations (123,547 new accounts in 2025), with 40.33% of new investors aged 21-30 and total unique CDS accounts reaching 740,639.

In bonds, combined debt and Sukuk securities trading reached TZS 5,860.68 billion in 2025 (+86.08%), and Tanzania's first Sharia-compliant Sukuk, issued in 2021, was oversubscribed by 36%.

The first Exchange Traded Fund (ETF) was listed in October 2025, and a second ETF launched in January 2026 (oversubscribed 540%) tracking large-cap EAC equities, while collective investment schemes' Net Asset Value reached TZS 2,686.0 billion in 2024 (+46.1%), with UTT AMIS dominating at TZS 4.3 trillion AUM across six funds and 420,682 investors (+88.8%).[12]

Insurance

Gross Written Premiums (GWP) reached TZS 1.52 trillion in 2024, up 20.2% from TZS 1.24 trillion in 2023, with an average annual growth rate of 10.8% over 2020-2024.[2]

By segment, general insurance accounted for 63.1% (TZS 957.2 billion), life insurance 20.4% (TZS 309.0 billion), health insurance 12.4% (TZS 187.5 billion), reinsurance TZS 374.3 billion, and microinsurance TZS 11.02 billion.

Takaful (Islamic) insurance grew 754.7% to TZS 4.6 billion in 2024 from TZS 0.5 billion in its 2023 launch year, while insurance penetration rose to 2.08% of GDP in 2024 (up from 2.01%), insurance density reached TZS 22,878 (+17.1%), and 25.9 million individuals were covered (39.2% of population).

As of 2025, Tanzania had 40 registered insurance companies—30 general (including two Islamic), six life, and four reinsurance—alongside 32 accredited foreign reinsurance companies.

SanlamAllianz Tanzania launched in October 2025 following the 2023 joint venture that created Africa's largest pan-African non-banking financial services group, while bancassurance contributed TZS 435.20 billion (37.7%) of intermediary GWP, emerging as a key distribution channel for Banks offering insurance products.

Social Security

Total social security assets reached TZS 21,353 billion in 2024, up 13.4% from TZS 18,834 billion in 2023, representing 7.6% of GDP.

Mandatory schemes covered 2,831,345 accounts in Mainland Tanzania (up from 2,799,344) and 139,235 in Zanzibar, functioning as pension funds, health insurance, and workers' compensation.

Member contributions totaled TZS 4,897.8 billion in 2024 (+11.8%), investment assets reached TZS 19,054.0 billion (+11.3%), and investment income reached TZS 1,328.5 billion (+9.7%).

The portfolio is diversified across Government securities, bank deposits, real estate (17%), equities (8%), and corporate bonds and other (12%), with 99.8% held domestically.

The rate of return on the total investment portfolio rose to 17% in 2024 (up from 9% in 2023), delivering a real return of 13.48% against inflation of 3.1%; the funding ratio for pension funds stood at 66.0% (above the 40% minimum) and the non-pension funding ratio at 4.1 times (above the 1.0 times floor).

Financial Inclusion

The Third National Financial Inclusion Framework (NFIF 2023-2028) is implemented under the National Council for Financial Inclusion.[14]

Adults accessing formal financial services rose from 86% in 2017 to 89% in 2023, while usage climbed from 65% to 76%, and the Tanzania Financial Inclusion Index (TanFiX) rose from 0.69 in 2023 to 0.81 in 2024.[15]

Mobile money active subscriptions reached 63.21 million in 2024 (+17.46% from 51.72 million in 2023), with transaction volume of 6,413.94 million (+26.73%) worth TZS 198,859.29 billion (+28.54%).

The Financial Sector Deepening Trust (FSDT) Tanzania highlights emerging technologies—blockchain, AI, and digital currencies—as drivers of further inclusion,[9] while the Bank of Tanzania is researching the feasibility of a central bank digital currency (CBDC), assessing population readiness, infrastructure, and policy implications.[10]

Specific NFIF interventions target women, youth, MSMEs, smallholder farmers, fishers, and persons with disabilities.

Development Finance Partners

Tanzania receives long-term development finance and technical support from a range of multilateral and bilateral institutions that anchor flagship infrastructure, health, agriculture, and financial-inclusion programs.

The AfDB financed the USD 272.12 million Msalato International Airport in Dodoma and co-funds Dar es Salaam BRT Phases III/IV/V, alongside agricultural and energy projects, while the World Bank anchored the Tanzania Mortgage Refinance Company (TMRC) under the Housing Finance Project, plus large-scale water, energy, education, and roads programs.

The IFC supports private sector investment across banking, manufacturing, agribusiness, and SME finance, often co-investing with local Banks, while the IMF provides sovereign-level macroeconomic surveillance, Article IV consultations, and Extended Credit Facility arrangements supporting Tanzania's reform agenda.

The AFD provides bilateral concessional financing across urban infrastructure, water, energy access, and sustainable agriculture; the EIB extends long-term loans for water, energy, transport, and SME finance lines through Tanzanian commercial Banks; and the AEF deploys risk-sharing and concessional debt facilities targeting SMEs and inclusive finance.

Policies

The Financial Sector Development Master Plan 2020/21-2029/30 sets nine strategic priorities, including financial inclusion, consumer protection, financial stability, long-term development finance, financial integrity, regional and international cooperation, research and innovation, capacity and ICT infrastructure, and modernization of the policy, legal, and regulatory environment.[13]

The Bank of Tanzania (BOT) is the primary regulator for Banks, financial institutions, microfinance, Islamic finance, fintech, and payment systems, operating under the Banking and Financial Institutions Act 2006 and associated regulations.

BOT transitioned from monetary aggregate targeting to an interest rate-based monetary policy framework in 2024, maintaining the Central Bank Rate at 5.75% for Q1 2026, and introduced a market-aligned system for Treasury bond coupon rates in January 2025, replacing the fixed-rate system to ensure rates reflect prevailing market conditions.

The Microfinance Act 2018 classifies providers into four tiers—Tier 1 microfinance Banks under standard banking laws, and Tiers 2-4 under specific rules including the Non-Deposit Taking Microfinance Service Providers Regulations 2019; fintech and payment systems are governed by the National Payment Systems Act, 2015 mobile payment guidelines, and the Fintech (Regulatory Sandbox) Regulations 2024 for innovation testing; and Islamic finance is regulated under the Banking and Financial Institutions (Non-Interest Banking Business) Regulations 2025.

Capital Markets are governed by the Capital Markets and Securities Act 1994 (as amended) and the Companies Act No. 12 of 2002, overseen by the CMSA—with DSE trading rules amended in June 2025 to improve liquidity, transparency, and investor protection; Insurance is regulated under the Insurance Act by the Tanzania Insurance Regulatory Authority (TIRA); and social security is governed by the Social Security Act, supervised by the Prime Minister's Office—Labour and Employment.

The Universal Health Insurance Act 2023 mandates health coverage for all residents, integrating existing schemes into a single system with mandatory contributions; the Finance Act 2025 introduced mandatory inbound travel insurance for foreign nationals entering Mainland Tanzania (excluding EAC and SADC residents) at a premium of USD 44 with coverage up to 92 days including medical care, evacuation, repatriation, and luggage; and the Anti-Money Laundering Regulations 2012 (amended 2019) ensure compliance across all regulated sectors.

Investment Opportunities

The SME financing gap stands out as a major entry point—MSME loans (including those accessed via personal credit) represented only 20.1% of total outstanding loans in 2024,[17] while SMEs contribute one-third of GDP and 40% of total employment.[16]

Barriers including informality, lack of collateral, low financial literacy, and high costs create openings for innovative lending solutions, alternative credit assessment, and tailored risk management products.

Islamic finance presents another growth avenue, supported by a large Muslim population and an expanding range of Islamic banking, investment, and Takaful products. Rising household financial assets—driven by higher incomes, broader credit access, and instruments such as green bonds, sustainable bonds, and sukuk—have expanded holdings in treasury bonds, equities, and collective investment schemes.[5]

Capital markets are scaling rapidly, with instruments supporting State-Owned Enterprises and sustainability-focused offerings, targeting 1 million investors by end of 2026 and 10 million by 2032.[19] Mobile money integration with the stock exchange drove a 397% increase in mobile trading registrations, with mobile-driven turnover reaching 24.3% of total equity trading.[18]

Insurance growth is anchored in digital transformation, regulatory reforms, the rollout of Universal Health Insurance, and the expansion of inclusive and microinsurance covering climate and specialized risks. Low awareness, underinsurance, and a shortage of demand-driven products create clear openings, while bancassurance—at TZS 435.20 billion (37.7%) of intermediary GWP—offers strong partnership opportunities for insurers and digital platforms.

Fintech opportunities span mobile payments, digital lending, savings, investments, and insurance products targeting underbanked segments through regulatory sandbox frameworks.

Development finance partners offer concessional capital, blended finance structures, and risk-sharing facilities for infrastructure, SME, and inclusive finance investments, providing a deep pool of co-investment capital for private players entering the market.

Last Update: May 2026

References

- https://www.bot.go.tz/Publications/Regular/Annual%20Report/en/2026022607584561.pdf (Guide reference #1)

- https://www.tira.go.tz/uploads/documents/en-New%20Annual%20Insurance%20Market%20Performance%20Report%202024.pdf (Guide reference #18)

- https://www.bot.go.tz/Publications/Regular/Monetary%20Policy%20Statement/en/2026020710260034.pdf (Guide reference #47)

- https://www.bot.go.tz/Publications/Regular/Quarterly%20Economic%20Bulletin/en/2026020820330341.pdf (Guide reference #66)

- https://www.bot.go.tz/Publications/Regular/Financial%20Stability/sw/2025072310063848.pdf (Guide reference #81)

- https://www.bot.go.tz/Publications/Regular/Financial%20Stability/en/2025072310063848.pdf (Guide reference #106)

- https://www.bot.go.tz/Publications/Other/Banking%20Supervision%20Annual%20Reports/en/2025090116315713.pdf (Guide reference #107)

- https://www.tanzaniainvest.com/wp-content/uploads/2026/03/Tanzania-banking-sector-Analysis-2025-By-AML-Finance.pdf (Guide reference #108)

- https://www.fsdt.or.tz/2024/11/29/digital-financial-services-and-financial-technology-in-tanzania/ (Guide reference #109)

- https://www.pwc.co.tz/press-room/navigating-uncharted-territory.html (Guide reference #111)

- https://www.tanzaniainvest.com/wp-content/uploads/2026/03/Dar-Es-Salaam-Stock-Exchange-Market-Performance-2025.pdf (Guide reference #112)

- https://www.instagram.com/p/DUL1KsnDIF1/?hl=en&img_index=1 (Guide reference #115)

- https://repository.mof.go.tz/items/7de714bd-8357-44ba-9fc9-b362890324d1 (Guide reference #117)

- https://www.fsdt.or.tz/wp-content/uploads/2023/10/NATIONAL-FINANCIAL-INCLUSION-FRAMEWORK-2023-2028.pdf (Guide reference #118)

- https://www.bot.go.tz/Publications/Regular/Annual%20Report/sw/2025082509110518.pdf (Guide reference #119)

- https://www.mof.go.tz/uploads/documents/en-1731921878-Final_FSDD%20ESMS_pdf.pdf (Guide reference #120)

- https://www.bot.go.tz/Publications/Regular/Annual%20Report/en/2025082509110517.pdf (Guide reference #121)

- https://dse.co.tz/storage/securities/DSE/financial_statement/Annual/PZFznv6PcCqY3s7h7hyLGLmHKoxcxu11OXxjL4pf.pdf (Guide reference #122)

- https://dailynews.co.tz/govt-dse-to-expand-capital-market-access (Guide reference #123)

Want to know more about Finance in Tanzania? Our free overview of the Tanzania Business and Investment Guide 2026 covers Finance, plus regulations, key sectors, and investment opportunities. The complete 141-page edition is also available for USD 99.

Download Free OverviewGet the Full Guide — USD 99