Mining

Tanzania's mining sector generated USD 4.1 billion in mineral exports in 2024, accounting for 25% of total exports, contributing 10.1% to GDP, and expanding by 9.8% in 2025.

In 2025, Tanzania was ranked the 4th most attractive destination for mining investment in Africa and the 3rd for mineral potential.[2]

The country hosts eight large-scale Mines—six for Gold and two for gemstones—alongside medium-scale operations and numerous small-scale Mines primarily producing Gold, Diamonds, and colored gemstones.[3]

Tanzania's mineral wealth spans three broad categories—metallic Minerals (Gold, silver, copper, Iron Ore, Nickel, tin, cobalt, Graphite, Rare Earth Elements), industrial minerals (gemstones including Diamonds, Tanzanite—unique to Tanzania—rubies, garnets, pearls, plus limestone, soda ash, gypsum, salt, phosphate, gravel, sand, dimension stones, and Helium), and energy minerals (Coal and Uranium).

The project pipeline is one of the most diversified in Africa, including the Kabanga and Dutwa Nickel projects, the Mantra Uranium project, the Mchuchuma and Kiwira Coal projects, the Liganga Iron Ore project, the Nyanzaga, Canaco and Nyakafuru gold projects, the Ngualla Rare Earth Elements project, and the Uranex Graphite project.

Tanzania has also established itself as a refining hub capable of processing up to 450 tonnes of gold annually, nearly half of Africa's total gold production.[10]

The Mwanza Precious Metals Refinery, opened in 2021, processes 960 kg/day at 99.99% purity, while the Geita Gold Refinery has received Responsible Minerals Initiative (RMI) certification on the path to London Bullion Market Association (LBMA) accreditation within three to five years.

Gold

Tanzania's estimated gold reserves stand at 45 million ounces, with annual production reaching 61.6 tonnes in 2024[4], positioning the country as Africa's eighth-largest gold producer and 19th globally.[5]

Operating large-scale gold mines include the Geita Gold Mine, North Mara Gold Mine, and Bulyanhulu Gold Mine—with North Mara and Bulyanhulu operated under the Barrick-Government Twiga Minerals joint venture.

Gold is Tanzania's second-largest export after tourism, contributing the vast majority of total mineral export value.

Gold sales reached USD 3.4 billion in 2024 (+11.8% from USD 3.0 billion in 2023), then climbed to USD 4.6 billion in 2025 (+37.4%), driven primarily by higher global gold prices.[1]

Silver is produced as a by-product of gold and copper deposits, mainly at Bulyanhulu and North Mara—9.8 tonnes worth USD 7.4 million in FY 2021/22.[6]

On value addition, the 2025/26 National Budget mandates that license holders sell at least 20% of gold locally for domestic processing, trading, or to the Bank of Tanzania, supporting refining capacity and national gold reserves.

Diamonds

Tanzania's estimated diamond reserves stand at 51 million carats, with production of approximately 373,000 carats in 2024[4], making it Africa's ninth-largest diamond producer and 11th globally.

The Williamson mine in Shinyanga is the primary producer—one of the oldest active mines in the world, holding 37 million carats of estimated reserves.

In the first nine months of 2025, approximately 284,000 carats of diamonds were produced, valued at USD 47.5 million.[7]

Tanzanite

The Mererani Hills near Mount Kilimanjaro is the sole source of Tanzanite globally—a blue-violet gemstone a thousand times rarer than diamond, with 50 million carats of confirmed reserves.

Tanzanite production reached 83,014 kg of rough and bead in 2024, with exports valued at USD 19.4 million.

Beyond Tanzanite, over 100 types of gemstones have been identified in Tanzania, with approximately 25 actively mined, including ruby, sapphire, garnet, emerald, spinel, tourmaline, alexandrite, tsavorite, the prized Winza ruby, and Mahenge spinel—primarily found in the Mozambique geological belt across Arusha, Mirerani, Tanga, and Morogoro.

Coal

Tanzania's estimated coal reserves total five billion tonnes.

Production reached 3.9 million tonnes in 2024 (+19.9% from 3.2 million tonnes in 2023), with a value of TZS 1,035.9 billion in 2024 (up from TZS 878.8 billion in 2023).

Growth has been driven by higher demand as an energy source in cement production domestically and in neighboring Burundi, Rwanda, Kenya, and Uganda.

In the first nine months of 2025, 2.3 million tonnes were produced, valued at USD 202.6 million.

Iron Ore

Iron Ore mining and iron production in Tanzania remain at an early stage of development but offer significant growth potential.

Substantial reserves are located in the Liganga area of Njombe Region, estimated at 126 million tonnes.

The Liganga Iron Ore Project envisions a planned production capacity of one million tonnes per year of steel products, plus approximately 175,400 tonnes of titanium and 5,000 tonnes of vanadium annually.[8]

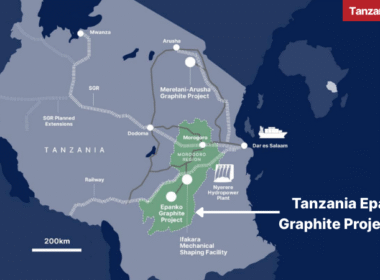

Graphite

Tanzania holds estimated Graphite reserves of 18 million tonnes, representing 6% of global graphite reserves—a vital component for producing anodes in lithium-ion batteries.[10]

The Lindi Jumbo Graphite mine in Ruangwa has an annual production capacity of 40,000 tonnes on a confirmed reserve of 5.5 million tonnes, with production expected to last 24 years.

The Mahenge and Epanko Graphite mines are each set to produce over 60,000 tonnes once operational, and Tanzania is projected to produce over 300,000 tonnes of Graphite annually within the next seven years.

Three Graphite projects are already in production—Lindi Jumbo Graphite (Lindi district), Permanent Minerals (Mirerani, Simanjiro district), and GodMwanga Graphite Project (Handeni district)—alongside six advanced Graphite projects ready for development in Ulanga, Nachingwea, and Lindi districts.[9]

Uranium

Tanzania's estimated Uranium reserves stand at 160 million tonnes, primarily located in the southern Mkuju River area and central regions such as Manyoni and Bahi.

There is no Uranium output currently—all projects remain at the exploration or development stage.

The major project is the USD 1.2 billion Mkuju River Project, led by Russian and Australian firms, which launched a pilot processing plant in 2025, with full-scale operations targeted for 2026-2029.

One Uranium project in Namtumbo district is among the 11 advanced critical-mineral projects ready for development as of 2023.[9]

Rare Earth Elements

Tanzania holds estimated reserves of 890,000 tonnes of Rare Earth Elements[11], including Nd-Pr metals (neodymium and praseodymium).

The most advanced project is the Ngualla Rare Earths Project, projected to produce 37,000 tonnes of REE metals annually, positioning Tanzania to become a top-five global producer.

The Wigu Hill REE project in Kilosa District holds deposits including lanthanum, cerium, neodymium, and praseodymium.

One Rare Earth Elements project in Songwe region is among the 11 advanced critical-mineral projects ready for development.[9]

Nickel, Cobalt and Lithium

Tanzania hosts world-class Nickel, cobalt, and limited Lithium deposits, primarily in Kabanga (East African Nickel Belt)—a geological zone rich in critical metals.

Kabanga is one of the world's largest undeveloped Nickel sulphide deposits, with estimated ore reserves of 52.2-58.0 million tonnes grading 1.98% Nickel, 0.27% copper, and 0.15% cobalt.[13]

Other Nickel projects include Kabulanywele, Kapalagulu, and Ngasamo Hill.

Cobalt occurs mainly as a by-product of nickel-copper sulphide deposits, with no standalone large-scale cobalt mines—it is associated with Nickel mineralisation at the Kabanga Nickel Project and at Kapalagulu.

Lithium is hosted mainly in hard-rock pegmatites and clay deposits in Dodoma and other central areas, with the Chenene Project as the main pipeline.

A multi-metal refinery is being developed for the Kabanga Nickel Project, with the final investment decision targeted for late 2026—it will produce battery-grade Nickel, copper, and cobalt.

Copper

Copper deposits are found in Mpwapwa, Dodoma, Chunya, Geita, and Mara, with exploration revealing high-grade ores of up to 46.3% Cu.[12]

Significant potential lies at Mpwapwa, Kinusi, Mbugani, and within the Ubendian Belt.

Commercial copper production remains limited and focused on small-scale mining.

Tanzania launched its first copper processing plant in 2025 in Chunya, handling 31,200 tonnes per month of low-grade ore (0.5-2% Cu) and producing 75% copper concentrate.

Helium

Tanzania hosts the world's largest known primary Helium deposit in the Rukwa Basin, with an estimated 5.7 trillion cubic feet.[14]

Two main projects are under development—the North Rukwa Project and the Southern Rukwa Project.

The North Rukwa Project could become the world's fourth-largest Helium reserve behind Qatar, USA, and Russia, with a prospective Helium resource of approximately 225.5 billion cubic feet.[15]

The Southern Rukwa Project is one of the few Helium projects globally not associated with hydrocarbons or CO2, positioning it within the 'green' Helium space—gross Helium contingent resources are evaluated at 296 million standard cubic feet, with potential to increase up to 1.35 billion.[16]

Industrial Minerals

Tanzania is endowed with industrial Minerals including asbestos, talc, ornamental and dimension stones, kaolin, phosphate, limestone, gypsum, diatomite, bentonite, vermiculite, carbon dioxide, salt, beach sands, and building materials such as stone aggregates and sand.

Most industrial mineral mines are operated by small-scale miners, with very few at medium scale.[17]

Key deposits include limestone in Tanga, Wazo Hill (Dar es Salaam), Lindi, and Mbeya—used in cement and agricultural soil amendment; gypsum in Itigi (Singida), Manda (Dodoma), Mkuranga (Coast), and Kilwa (Lindi) for boards and cement; soda ash at Lake Natron (Arusha) for glass, cement blocks, and road construction; and phosphate at Minjingu (Manyara) and Nachingwea (Lindi) for agriculture and local soap production.

Clay deposits in Pugu (Dar es Salaam), Bagamoyo (Coast), Moshi (Kilimanjaro), and Kondoa (Dodoma) support burnt bricks, roofing tiles, and pottery, while marble and granite from Kilimanjaro, Dodoma, Mbeya, and Morogoro feed flooring, walls, granite tiles, and countertops for domestic and export markets.

Policies

The Ministry of Minerals (MOM) governs the sector, having been separated from the Ministry of Energy in 2017.

The Mining Act 2010 is the principal legislation—regulating prospecting, mining, mineral processing, and trading, affirming sovereignty of the people of Tanzania over natural resources, and establishing the Mining Commission to supervise the sector and issue, renew, or cancel mineral rights.

The Mining Act amended in 2017 introduced a mandatory 16% non-dilutable free-carried Government interest in all mining projects, deepened local participation, and stimulated local value addition.

The 2019 amendment allowed the Government to raise its free-carried interest up to 50%.

Mining Vision 2030, introduced in 2024, aims to increase wealth creation from mining, expand opportunities for women, youth, and people with special needs, and expand geological knowledge through a high-resolution airborne geophysical survey targeting at least 50% national coverage by 2030 (up from 16% currently).[18]

Royalties are set at 6% on gold, metallic minerals, rough colored gemstones, and rough diamonds (4% if gold sold to BOT, 2% if sold to local refineries); 5% on Uranium; 3% on Coal (1% if sold to domestic industries), industrial minerals, and building materials; and 1% on salt, phosphate, cut and polished diamonds and gemstones.[19]

A 1% clearance and inspection fee applies to all minerals except salt and gold sold to refineries, and the Finance Act 2025 added a 0.1% HIV Response Levy on gross mineral value.

The Local Content Regulations 2018 (amended 2019, 2022, 2025) require that indigenous Tanzanian companies (at least 20% Tanzanian equity, 80% Tanzanian senior management, 100% Tanzanian non-managerial staff) be prioritized for goods and services, while foreign suppliers must form joint ventures with 100% Tanzanian-owned companies holding at least 20% equity.[20]

The 2022 amendments extended obligations to law firms, telecoms, banks, and caterers, and the 2025 amendments listed 20 goods and services reserved exclusively for 100%-Tanzanian-owned indigenous companies.

The Mining (Corporate Social Responsibility) Regulations 2023 require mineral rights holders to prepare an annual CSR plan addressing environmental, social, economic, and cultural priorities aligned with host community needs.

Small-Scale Miners have seen their share of mining sector revenues rise from approximately 5% before the 2017 Mining Act amendments to nearly 40% in FY 2022/2023.[21]

The Mining (Technical Support to Small Scale Miners) Regulations 2025 establish a dedicated technical support framework for Primary Mining License holders, STAMICO is acquiring 15 drilling rigs to support small-scale miners, and TZS 187 billion was disbursed to small-scale miners between July 2023 and March 2024.[18]

On value addition, Mining Act amendments require miners to reserve and process a portion of output domestically, and the 2025/26 Budget mandates that license holders sell at least 20% of gold locally to refiners, smelters, jewelers, or the Bank of Tanzania.

Since 2019, the Government has set up 44 mineral markets and 120 buying centers nationwide[23], while international gemstone auctions were reintroduced in late 2024 by the Mining Commission and Tanzania Mercantile Exchange via an electronic sales system.

Investment Opportunities

Mineral exploration in new prospective areas is opening up as high-resolution airborne geophysical survey coverage expands from 16% to at least 50% of the country by 2030, de-risking greenfield targets for incoming explorers.

Mineral processing plants for ore preparation and concentration ahead of smelting or refining are a major frontier, particularly for critical minerals where licences now require a domestic value-addition plan. Gold refineries and other smelting and refining facilities also offer entry points, with Tanzania's 450 tonnes/year refining capacity — nearly half of Africa — and the path to LBMA accreditation supporting institutional gold supply.

Base metals mining and processing (including platinum group metals) and beneficiation of industrial minerals such as lime, soda ash, kaolin, gypsum, coal, iron ore, and dimension stones remain underexploited at scale.

Gemstone cutting and polishing (lapidary), rock and mineral carving, and jewellery manufacturing using gold, precious metals, and gemstones are high-value-add activities reserved for Tanzanian participation, with upcoming digital gemstone auctions reinforcing the country's positioning as a regional gem trading hub.

Geochemical and mineral testing laboratories are a priority sector, with new modern testing facilities under construction in Dodoma, Geita, and Chunya to anchor a regional research hub[22]. Mineral trading and marketing opportunities run through 44 mineral markets and 120 buying centres nationwide.

Mining services — drilling, supply of explosives, grinding media, and mill liners — plus joint ventures with Tanzanian entrepreneurs under Local Content Regulations offer steady entry routes for specialist operators.

Mining-related infrastructure such as roads, ports, and power solutions for remote operations is particularly relevant for the Kabanga Nickel multi-metal refinery (FID targeted late 2026) producing battery-grade nickel, copper, and cobalt, and the Liganga Iron and Steel smelting complex in Njombe.

Last Update: May 2026

References

- https://www.bot.go.tz/Publications/Regular/Monthly%20Economic%20Review/en/2026020312553210.pdf (Guide reference #12)

- https://www.fraserinstitute.org/sites/default/files/2026-02/annual-survey-of-mining-companies-2025.pdf (Guide reference #140)

- https://www.madini.go.tz/media/United_Republic_of_Tanzania_Investor_Guide..pdf (Guide reference #141)

- https://www.mof.go.tz/uploads/documents/en-1757496956-ECONOMIC%20SURVEY%20BOOK,%202024%20SEPT_SENT%20FINAL.pdf (Guide reference #142)

- https://www.gold.org/goldhub/data/gold-production-by-country (Guide reference #143)

- https://www.tumemadini.go.tz/media/uploads/annual_reports/2025/01/14/Mining-Commission-Annual-Report-2021-2022-New.pdf (Guide reference #144)

- https://www.bot.go.tz/Publications/Regular/Quarterly%20statistical%20Bulletin/en/2025110513234194.pdf (Guide reference #145)

- https://ndc.go.tz/iron-steel/ (Guide reference #146)

- https://eiti.org/sites/default/files/TEITI%2015TH%20EITI%20REPORT.pdf (Guide reference #147)

- https://manufacturingafrica.org/wp-content/uploads/2025/09/Tanzania-Minerals-Value-Addition-Perspective_Core-Report.pdf (Guide reference #148)

- https://pubs.usgs.gov/periodicals/mcs2024/mcs2024-rare-earths.pdf (Guide reference #149)

- https://baridigroup.com/baridi-group-identifies-significant-copper-deposits-in-mpwapwa-tanzania/ (Guide reference #150)

- https://ir.lifezonemetals.com/news/press-releases/news-details/2025/Lifezone-Metals-Files-the-Feasibility-Study-Technical-Report-Summary-for-the-Kabanga-Nickel-Project-in-Tanzania/default.aspx (Guide reference #151)

- https://noblehelium.com.au/wp-content/uploads/2022/04/Helium-In-Tanzania-Linked-File.pdf (Guide reference #152)

- https://api.investi.com.au/api/announcements/nhe/cc9335db-f0c.pdf (Guide reference #153)

- https://polaris.brighterir.com/public/helium_one/news/rns/story/xz461ow (Guide reference #154)

- https://www.madini.go.tz/media/Tanzania_Mining__Investment_Conference_2024.pdf (Guide reference #155)

- https://www.madini.go.tz/page/03cef72a-bdd3-41dc-ba84-40954095b835/ (Guide reference #156)

- https://www.tumemadini.go.tz/pages/mineral-royalties-and-inspection-fees-rates/ (Guide reference #157)

- https://www.tumemadini.go.tz/pages/local-content-csr-monitoring/ (Guide reference #158)

- http://madini.go.tz/page/60cc4e29-40e0-415c-b088-0cc95996a557/ (Guide reference #159)

- https://www.madini.go.tz/media/MADINI_BULLETIN.pdf (Guide reference #160)

- https://www.tumemadini.go.tz/statistics/list-of-mineral-markets (Guide reference #161)

Want to know more about Mining in Tanzania? Our free Tanzania Business and Investment Guide 2026 covers Mining, plus regulations, key sectors, and investment opportunities—all in one place.

Download Free Guide